Reading time: about 10 minutes. Five real, public commission disputes and what each one teaches Sales Ops, Finance, and HR. All cases drawn from court records, regulatory filings, and reporting in Reuters, Bloomberg, the Wall Street Journal, and similar outlets.

Every commission plan looks fine on a slide. Every commission disaster looks obvious in hindsight. The cases below are what happens in the gap between those two states. None of them came from small or careless companies. They came from large enterprises with lawyers, audit committees, and competent finance teams. The lesson is not that they were unusual. The lesson is that any growing sales organization is one bad assumption away from sitting on the same kind of headline.

Case 1: Wells Fargo and the incentive plan that became a scandal (2016 – 2020)

What happened: Aggressive cross-sell incentives at Wells Fargo branches drove employees to open millions of unauthorized customer accounts to hit sales targets. The structure paid for activity (account openings) rather than outcomes (legitimate customer relationships).

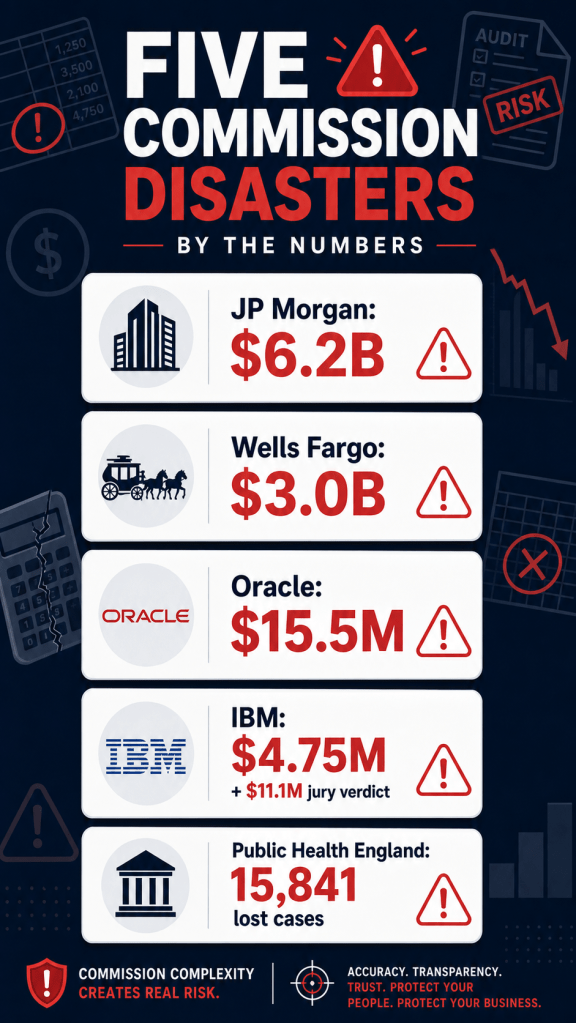

The numbers: Wells Fargo paid $185 million in regulatory penalties in 2016 and an additional $3 billion in 2020 to settle related criminal and civil investigations. More than 5,000 employees were terminated.

The lesson: Pay for the right outcome. If you pay for activities rather than results, you will get the activity, including the kinds you do not want. Build retention, customer satisfaction, or contract value into the plan, not just gross unit count.

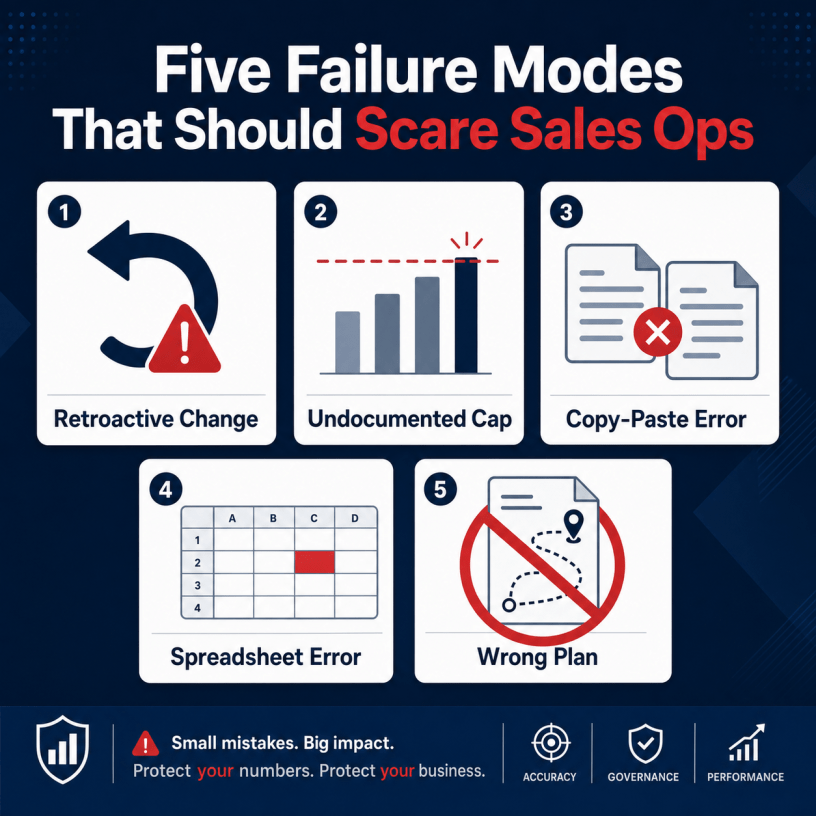

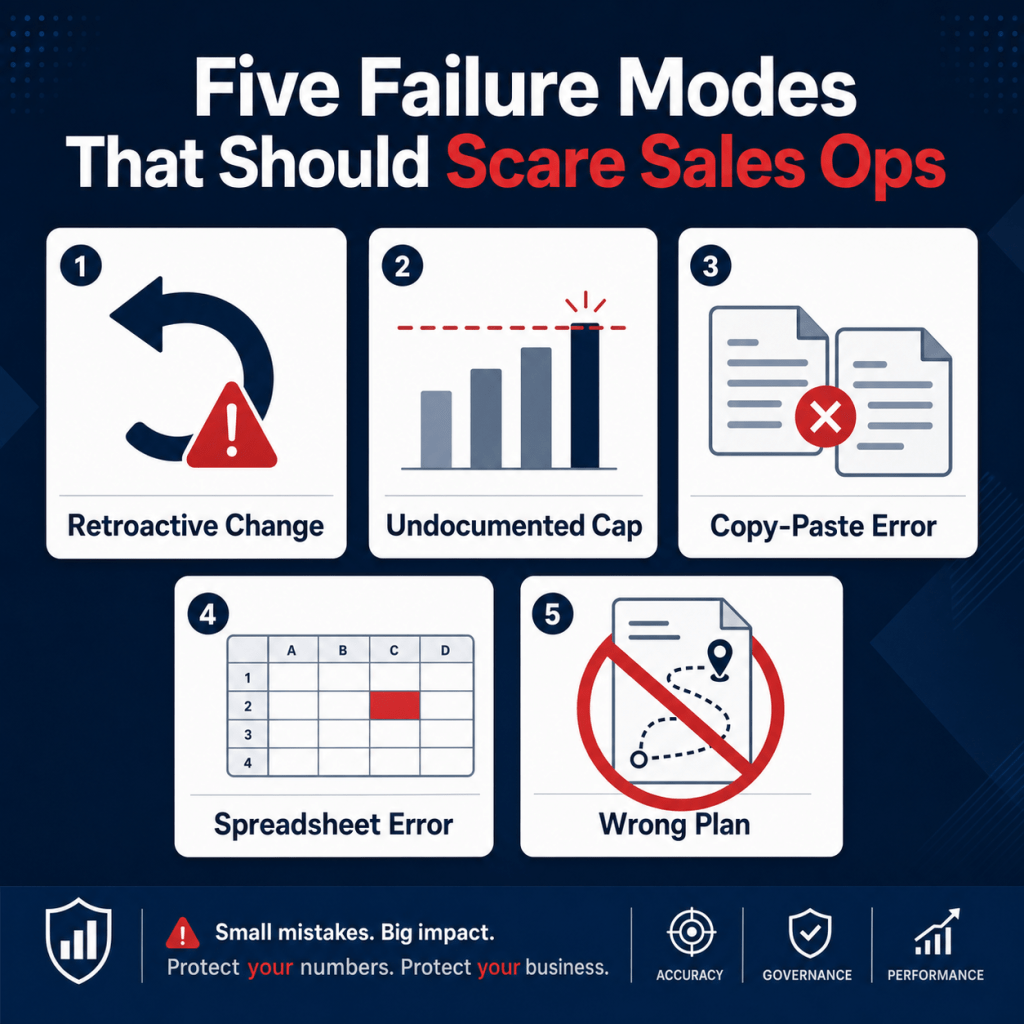

Case 2: JP Morgan and the spreadsheet that lost $6.2B (2012)

What happened: The London Whale trading loss is most often discussed as a derivatives story, but the proximate cause was a spreadsheet. A copy-paste error in the bank’s Value-at-Risk model meant traders were operating with a risk number roughly half the correct figure. By the time the error was discovered, positions were too large to unwind without enormous losses.

The numbers: Total losses exceeded $6.2 billion. The bank paid more than $1 billion in fines to regulators. JP Morgan’s own internal task force report and the Senate Permanent Subcommittee on Investigations both pointed to spreadsheet model risk as a root cause.

The lesson: “It’s just a spreadsheet” is the most expensive sentence in finance. Anywhere money flows on the back of a workbook, you have a model that needs the same controls as code: version control, test cases, and a system of record. Commission plans are no exception.

Case 3: Oracle’s $15.5M PAGA settlement (2015 – 2025)

What happened: In Abrishamcar v. Oracle, plaintiffs alleged that Oracle’s commission practices, including retroactive plan changes and clawbacks, violated California labor law. The case was filed in 2015 and worked through state and federal courts for nearly a decade. Public reporting indicates the case affected more than 5,000 California employees.

The numbers: The case ultimately settled for $15.5 million in February 2025, structured under California’s Private Attorneys General Act. A separate Oracle case (Johnson, 2017) involved a $150 million class action over commission formula changes.

The lesson: Retroactive plan changes are legally radioactive in many jurisdictions. If you need to change a plan, change it forward, with effective dates and explicit rep acknowledgement. Document every change. Treat the commission plan as a contract, because to a court, it often is.

Case 4: IBM and the $11.1M Kingston verdict (2021 – 2023)

What happened: Multiple commission disputes have been litigated against IBM. In Kingston v. IBM, a federal jury awarded the plaintiff $11.1 million, which included $113,000 in unpaid commissions plus damages and fees. A separate California class action settled for $4.75 million in 2023 covering approximately 1,500 California sales reps. Public reporting referenced approximately $43.4 million IBM had previously withheld from commissioned reps.

The lesson: Commission caps and “subject to management discretion” language do not survive courtroom scrutiny when reps relied on a documented plan to take the job. If a rep books the deal under one set of rules, you owe them that set of rules. Document discretion narrowly and use it sparingly.

Case 5: Public Health England and the row limit nobody checked (2020)

What happened: During the COVID-19 pandemic, Public Health England used Excel to aggregate test results for contact tracing. The system used the legacy XLS format with a 65,536-row limit. When the limit was hit, the rows simply stopped being written. 15,841 positive cases were lost from the contact tracing system over an eight-day window.

The lesson: This is a public health story, not a commission story, but the structural failure is the same. Spreadsheets have invisible limits that nobody notices until they bite. Row limits, character limits, formula precision limits, and most dangerously, the limit of one human being’s ability to remember every formula in a 40-tab workbook. When the workbook is the system of record, the workbook is the risk.

The pattern across the five

| Case | Root cause | What would have prevented it |

|---|---|---|

| Wells Fargo | Plan paid for the wrong outcome | Multi-measure plan with retention and customer satisfaction |

| JP Morgan | Spreadsheet model risk | Calculation in a tested system of record |

| Oracle | Retroactive plan changes | Effective-dated rules and rep acknowledgement |

| IBM | Discretionary caps not in plan documents | Explicit, documented plan with no surprises |

| Public Health England | Spreadsheet hit a silent limit | Purpose-built data system, not Excel |

What good looks like, drawn from what bad looked like

- Pay for outcomes, not activity. If the plan can be gamed, it will be.

- Treat the plan as a contract. Document every rule, every cap, every clawback, in plain English.

- Effective-date everything. Changes apply to deals booked after the change date, never before.

- Move calculation off spreadsheets. A system of record with audit trail, version control, and immutable history.

- Make rep statements transparent. Drill-down to deal level. If a rep cannot understand the calculation, the dispute is already on its way.

- Test plans against real data before launch. Run the new plan against the last four quarters of bookings and surface the surprises before reps do.

The economics of getting it wrong

The headline number on a commission lawsuit is the settlement, but the real cost is bigger. Across the five cases above, the consistent ancillary costs are: years of senior management distraction, regulatory and legal fees, employee morale damage, retention crisis among top performers, public brand impact, and SOX or audit committee scrutiny that lingers for years afterward. The settlement is the visible part of the iceberg.

The companies that avoid this category of pain do not get there by being lucky. They get there by treating commission as a controlled financial process, the same way they treat revenue recognition, payroll, and tax.

Bottom line

Commission disasters do not come from rate decisions. They come from process and documentation gaps that were obvious in hindsight. The fix is uninteresting and effective: clear plans, effective-dated rules, automated calculation, immutable history, and a culture that treats the plan as the contract it is. Boring, until you read about the company that did not.

Want to see what a controlled commission process looks like in practice? Book a Sales Cookie demo or browse the Sales Cookie blog for more on commission management.

Sources: U.S. Department of Justice (Wells Fargo); CFPB Wells Fargo enforcement; SEC London Whale order; The Recorder, Oracle PAGA settlement (2025); Daily Business Review, IBM California class action (2023); BBC, PHE Excel error (2020).