Reading time: about 11 minutes. A practical playbook on SPIF and bonus program design, with the structures that move the number, the ones that do not, and the operational gotchas that quietly cost real money.

Every sales leader has run a SPIF that worked. Every sales leader has also run one that paid out a lot of money for behavior that would have happened anyway. The difference between the two outcomes is rarely the rate. It is whether the SPIF was tied to a behavior that actually changed because of the program, with measurement set up before kickoff. This guide walks through SPIF anatomy, when to use them, when to change quota instead, the tax treatment everyone forgets, and the failure modes that cost money without moving the number.

What SPIF actually means

SPIF (sometimes “spiff”) is widely understood as a Sales Performance Incentive Fund, a temporary cash incentive layered on top of regular commission to move a specific behavior in a specific window. The term has been in continuous use in U.S. sales since at least the 1940s, predating most of the technology you would associate with modern sales comp. It is essentially a focused, short-duration override.

SPIFs do three things well: they shift attention to a slow-moving product line, they push deals into a closing window, and they break ties in vendor selection when reps can sell more than one product. They do four things badly: they create perverse incentives, they get gamed, they over-pay for behavior reps would have done anyway, and they fragment plan documentation if not retired cleanly.

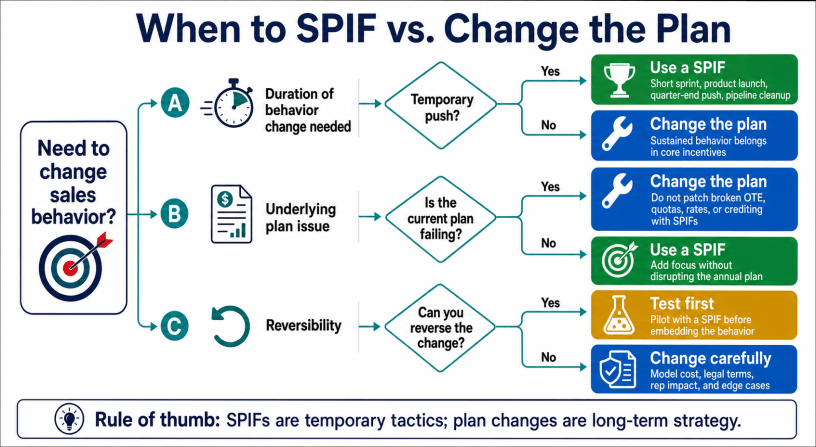

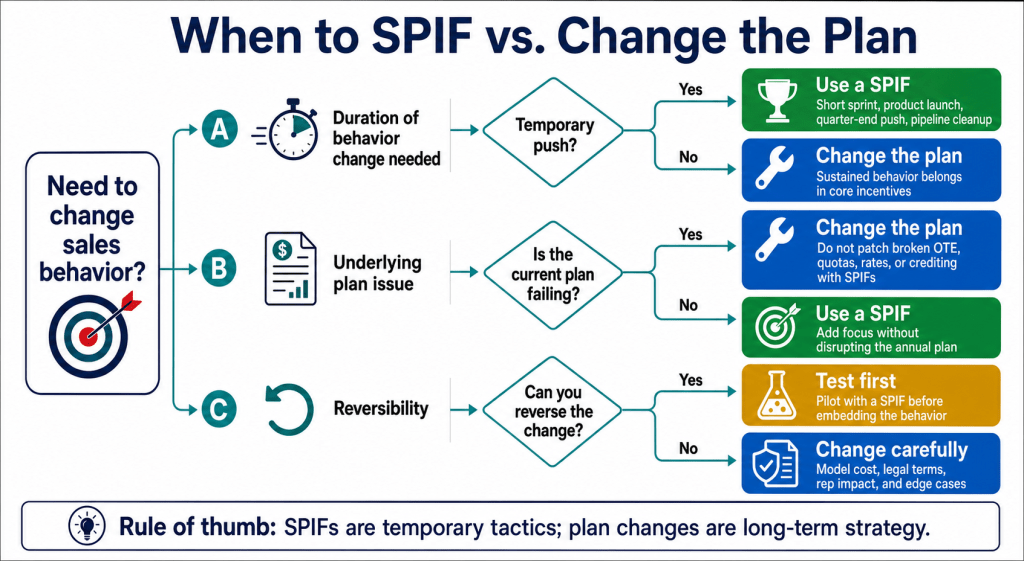

SPIF vs. quota change vs. plan redesign

| Lever | Use when | Risk |

|---|---|---|

| SPIF | You need to shift behavior for 30 to 90 days | Distortion of base plan if extended |

| Quota change | The market or product changed structurally | Mid-year quota changes erode trust |

| Plan redesign | Ongoing misalignment between rep behavior and outcomes | Slow to take effect; high change cost |

| Manager push | The behavior change is short-term and informal | Inconsistent across teams |

SPIFs are the right tool for a narrow class of problems. Most plan complaints look like SPIF candidates and are actually plan-design problems in disguise.

Five SPIF designs that actually work

1. Product push SPIF

Goal: Move a specific product or SKU. Design: Flat dollar bonus per unit sold, time-bounded. Example: $250 per attached Service Agreement closed in March.

Why it works: Clear, fast, easy to track. Reps know exactly what behavior pays.

2. End-of-quarter close SPIF

Goal: Pull deals across the line in the last 10 days of a quarter. Design: Increased rate (e.g., 1.5x base commission) on deals that close before quarter-end with full payment terms.

Why it works: Reps already want to close in-quarter. The SPIF accelerates the marginal deal that would have slipped.

3. New logo SPIF

Goal: Refocus reps on net-new accounts when expansion has dominated. Design: Bonus on first deal with a customer that has not transacted in 12+ months. Tiered if multiple new logos in the window.

Why it works: New logo motion is harder than expansion; the bonus reflects the difficulty.

4. Pipeline build SPIF

Goal: Increase top-of-funnel before a slow quarter. Design: Bonus per qualified opportunity created and accepted by sales leadership, with a quality bar (minimum size, decision-maker contacted).

Why it works: Aligns leading indicator with revenue outcome. What to watch: Quality bar must be enforced or volume crowds out conversion.

5. Multi-product attach SPIF

Goal: Increase cross-sell of multiple SKUs in a single deal. Design: Multiplier on commission when a deal includes both Product A and Product B. Example: 1.25x commission on bundled deals.

Why it works: Slight pull toward bundling without distorting the base plan. What to watch: Reps will discount Product B to land the bundle; pair with a price floor.

Five SPIF designs to avoid

- The “kicker that becomes permanent.” A SPIF that is renewed quarter after quarter is no longer a SPIF, it is the plan. Roll it into base commission.

- The opaque SPIF. Reps cannot calculate what they earn. They will not change behavior for a payout they cannot model.

- The “qualifies in retrospect” SPIF. Adding eligibility criteria after deals close. Equivalent to retroactive plan changes; legally fragile and rep-trust corroding.

- The single-rep SPIF. A SPIF nominally available to all but realistically winnable by one rep due to territory or pipeline. Read as favoritism.

- The product-push SPIF on a product reps cannot actually sell. If reps would already attach if they could, the SPIF will not help. Diagnose the sales-readiness problem first.

Tax treatment everyone forgets

SPIFs paid to W-2 employees are wages and must run through payroll, with all applicable income tax, FICA, and Medicare withholding. SPIFs paid to non-employees (channel partners, third-party reps) are typically reported on 1099-NEC if they exceed the IRS reporting threshold. The mistake to avoid: paying a SPIF as a “bonus check” outside payroll. The IRS has been explicit since at least 2008 that SPIFs to employees are wages regardless of how they are labeled or distributed. If a partner-reseller’s reps receive SPIFs from the manufacturer, the manufacturer typically issues 1099-NEC.

| Recipient | Tax form | Treatment |

|---|---|---|

| Direct employee | W-2 | Wages; full payroll withholding |

| Independent contractor (1099) | 1099-NEC | Reportable nonemployee compensation |

| Channel partner rep (third-party) | 1099-NEC from manufacturer | Common for OEM SPIFs |

| Non-cash awards (gift cards, trips) | W-2 fair market value (employees) or 1099 (non-employees) | Still taxable; document FMV |

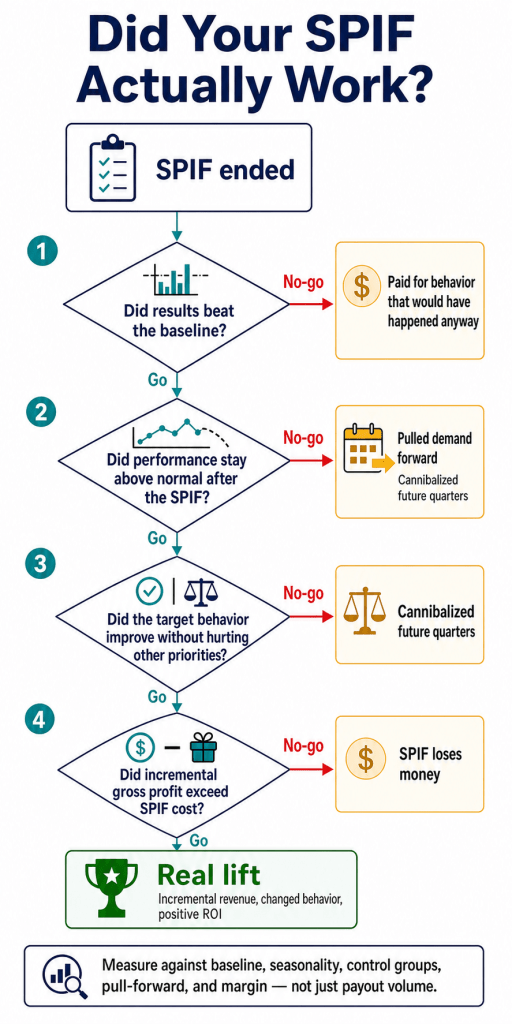

Measuring whether the SPIF worked

Most SPIFs are evaluated by total payout (a vanity metric) and total revenue in the SPIF window (correlation, not causation). A defensible measurement framework asks four specific questions:

- Counterfactual. Compare the SPIF window to a similar prior period without a SPIF. Did the behavior actually change? Watch for natural seasonality.

- Marginal vs. base. How much of the behavior would have happened anyway? Subtract the trailing-period baseline.

- Reversion. What happened in the period immediately after the SPIF ended? A drop below baseline means reps cannibalized future activity.

- Cost-per-incremental-deal. SPIF dollars paid divided by deals incrementally won. If this number exceeds the gross margin per deal, the SPIF lost money.

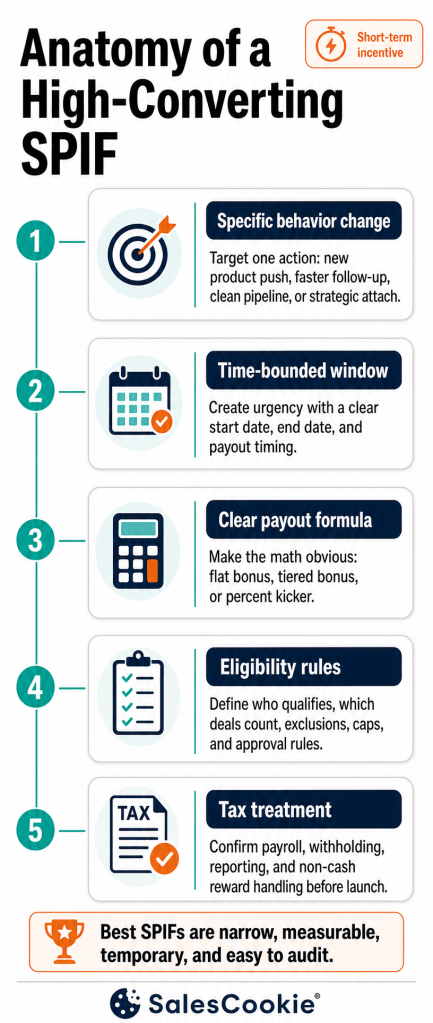

Operational checklist

| Check | Why it matters |

|---|---|

| SPIF documented in writing before kickoff | Avoids “I didn’t know” disputes and meets state wage law requirements |

| Eligibility rules explicit (which reps, segments, products) | Removes favoritism perception |

| Start and end dates clearly stated | Prevents trailing claims after window closes |

| Calculation formula stated in plain language | Lets reps model their own outcome |

| Tracked in the same system as base commission | Avoids parallel spreadsheet drift |

| Pre-defined success metric and baseline | Enables real measurement after the fact |

| Sunset condition explicitly stated | Prevents “permanent SPIF” drift |

What good looks like in practice

A well-run SPIF program at a 50-rep B2B SaaS company looks like this. Two SPIFs per quarter, never more. One product-focused, one motion-focused (close acceleration or pipeline build). Each documented in a one-page brief signed off by the CRO and the CFO. Each tracked in the commission system as a separate line item, attached to the same deal records as base commission. Each measured against the prior trailing four-week baseline before declaring success or failure. Each retired cleanly at the end-date with a write-up showing what happened.

The companies that do this never face the “why are we still paying that SPIF” conversation in November. They also never face the rep-trust hit when a SPIF gets retroactively re-interpreted at month-end.

Bottom line

SPIFs are a precision instrument. Used well, they nudge specific behaviors for short windows at modest cost. Used poorly, they pay a lot of money for things that would have happened anyway and erode the integrity of the base plan in the process. The discipline is unglamorous: write it down, time-box it, measure it against a baseline, and retire it cleanly. Most SPIF problems are documentation problems wearing different hats.

Manage SPIFs in the same system as base commission. Sales Cookie tracks SPIF programs alongside base plans with full audit trail and rep statement transparency. Read our companion guides on commission structures and closing the trust gap on commissions.

Sources: IRS Form 1099-NEC instructions; IRS Publication 15 (Employer’s Tax Guide); WorldatWork incentive design research; Salesforce State of Sales 2024.