Reading time: about 14 minutes. How to design commission plans that survive retroactive sales data changes, mid-period amount edits, and the inevitable true-up at month-end. Written for Sales Ops leads tired of explaining why January’s number changed in March.

Most commission plans assume sales data is final once a deal is closed. In real life sales data is never final. Deal amounts change when contracts are renegotiated. Close dates move when finance reclassifies revenue. Refunds and credit memos arrive weeks later. Orders are split or merged. Customers downgrade. CRM administrators correct a misclassified opportunity. Every one of these events forces the question: do we re-pay the commission, claw it back, true it up, or freeze the original number? Without a deliberate policy and a system that supports it, the answer is whatever the analyst can keep straight in their head, which is the source of the worst commission disputes.

This is the design guide for handling retroactive sales data and the true-ups that follow. We cover the three structural patterns Sales Cookie recommends, when to use deductions, how to prevent double-payment, and the rep-statement language that keeps a true-up from feeling like a clawback.

Why sales data changes (and why you cannot pretend it does not)

The most common retroactive-change scenarios:

- Amount adjustments. A $100K deal becomes a $92K deal because a discount was applied after close. Or a $50K renewal becomes $65K because an add-on was processed in the same record.

- Refunds and credits. A customer is refunded part of an invoice in a later period. The commission paid in the original period now reflects revenue that no longer exists.

- Date corrections. A deal initially booked in March is reclassified to April by finance for revenue recognition reasons. The rep who got paid an accelerator in March no longer qualifies because the deal no longer belongs to March.

- Ownership changes. A deal is reassigned to a different rep after close, either because of a territory dispute or a transfer.

- Status reversals. A deal marked won is later reverted to open or lost.

- Quota and rate changes. A plan is restructured mid-year. Past calculations done under the old plan have to be either grandfathered or rerun under the new plan.

Each of these creates the same fundamental problem: a calculation that produced a number in March is now wrong, given what we know in May. The question is not whether to react. The question is which of three reaction patterns to use, and that choice should be made deliberately, plan by plan, not improvised cycle by cycle.

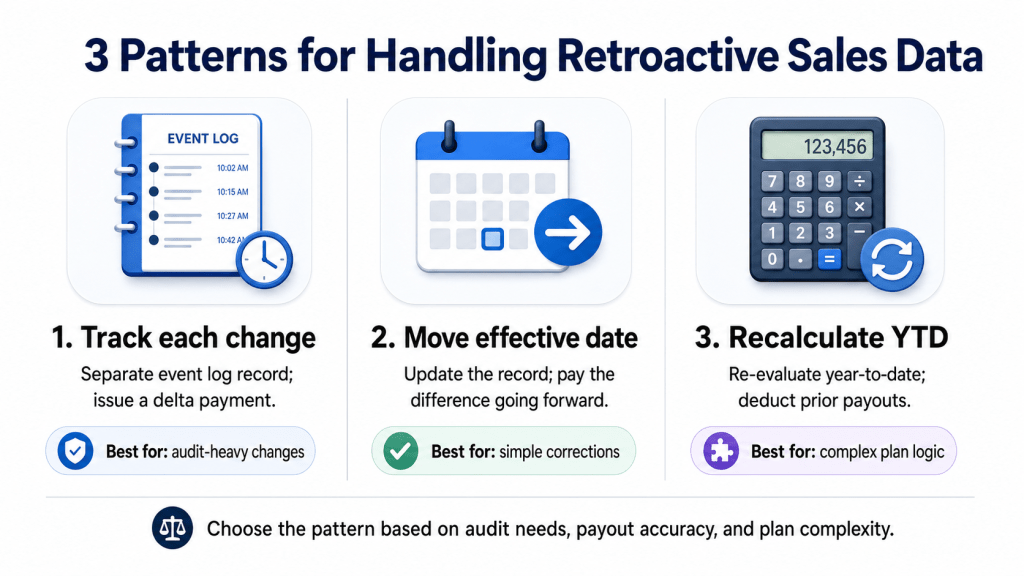

Pattern 1: Track each change as a separate record

This is the cleanest pattern from an audit standpoint. Every time a deal’s amount, date, or owner changes, the CRM or billing system writes a new record rather than overwriting the existing one. The transaction history becomes an event log: a sequence of immutable rows, each with its own effective date.

Example: order ID-123 starts at $40K in January, gets adjusted to $35K in February, then to $50K in March. Three records exist in the system, each timestamped, each independently visible. When Sales Cookie calculates commissions for any given period, it looks up everything previously paid against this deal and issues only a delta amount, sized to bring the cumulative payout in line with the latest record. Per the Sales Cookie KB on ever-changing data, this is the recommended approach when you can structurally support it because it produces the cleanest paper trail and is the easiest to explain to an auditor.

If the source system does not produce unique IDs for these records natively, Sales Cookie can synthesize one by combining fields. The standard convention is [Date] + [Order ID], which gives each amount snapshot a distinct identity. The deduction logic then works correctly because the engine can match prior payouts to the current record version.

| When this fits | When this does not fit |

|---|---|

| CRM or billing system natively writes amendment records | CRM only stores the current state of an opportunity |

| You need the strongest audit trail (SOX, regulated industries) | Volume of amendments is so high that the event log becomes unmanageable |

| Each change has a meaningful effective date | You want a single rep-facing line item per deal regardless of history |

Pattern 2: Update the record and move the effective date forward

This pattern applies when you cannot track each change as a separate record because the source system only stores the current state. There is one opportunity record per deal, and that record is updated in place when the amount changes. To keep commissions correct without producing an explicit event log, the convention is: every time the amount changes, also move the effective date forward to the day of the change.

Example: a deal closes in January at $40K. In February the amount is corrected to $35K, and the effective date is updated to February. In March it changes again to $50K, effective March. Each subsequent monthly calculation re-processes the same record, but because the effective date has moved forward into the current period, the engine treats it as a new event to credit and uses prior payouts as a deduction baseline. The rep ends up with the right cumulative total, just without the explicit amendment log.

There is an honest limitation worth flagging: with this pattern, you cannot reconstruct what commissions would have been “as of” a historical point in time, because the underlying data has already been overwritten. As long as you only need calculations to roll forward, that is fine. If your auditor needs point-in-time reproducibility, this pattern is the wrong choice.

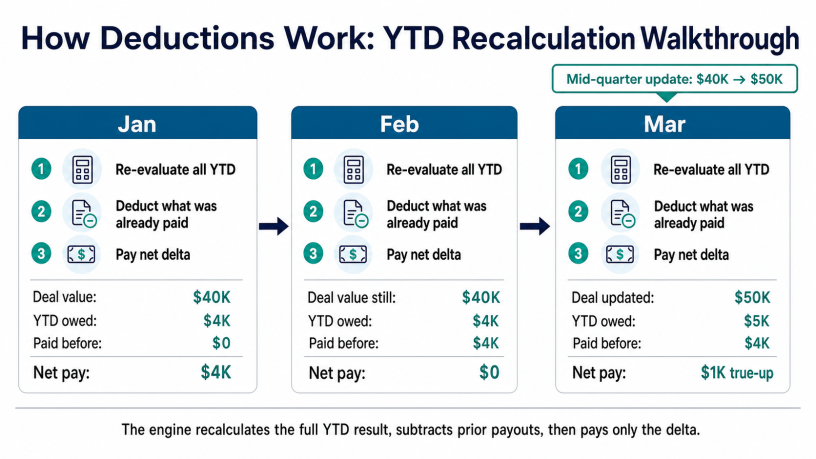

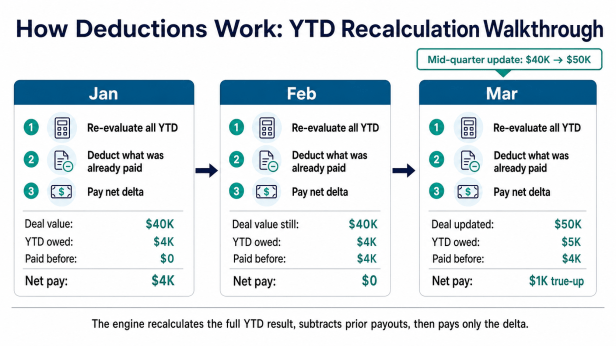

Pattern 3: Update the record, do not change the effective date, recalculate with deductions

The third pattern applies when neither of the above is possible. There is one record per deal, the amount can change at any time, and the effective date is locked (for example because it is the Closed Date and finance does not allow it to be moved). The fix is to switch the plan from period-based calculation to year-to-date or quarter-to-date recalculation, paired with deductions for what has already been paid.

Every month, the plan re-evaluates all YTD commissions against the latest data, then automatically deducts what has already been paid in earlier months. The rep ends up with a cumulative YTD payout that matches the latest version of the data, and the engine’s deduction logic prevents double-payment when calculation periods overlap. Per the Sales Cookie KB on deductions, this is the standard mechanism for absorbing retroactive change while preserving cash already paid.

| Period | YTD recalculation | Already paid | Net payout this period |

|---|---|---|---|

| January (deal closes at $40K) | $4,000 | $0 | $4,000 |

| February (no change) | $4,000 | $4,000 | $0 |

| March (deal amount corrected to $50K) | $5,000 | $4,000 | $1,000 true-up |

| April (refund: $50K down to $30K) | $3,000 | $5,000 | ($2,000) clawback applied as deduction |

Monthly plan with QTD attainment: the practical case

One of the most common variants of this pattern is a monthly plan with quarter-to-date attainment. The rep is paid every month, but attainment (and therefore the rate they earn) is measured against quarterly quota. This is a common SaaS pattern: pay frequently to keep cash flow steady for the rep, but measure performance over a window long enough to smooth out monthly noise.

Per the Sales Cookie QTD attainment recipe, there are two valid configurations:

| Setting | With deductions | Without deductions |

|---|---|---|

| Plan period | Monthly | Monthly |

| Start date override | Quarter start (set in advanced options) | Quarter start (set in advanced options) |

| QTD attainment | Yes | Yes (advanced option) |

| Per-transaction reward formula | Process all QTD transactions; engine deducts previously-paid commissions | Process only current-period transactions; deduction not applied |

| Cash bonuses at attainment levels | Supported | Supported |

| Mid-quarter rate change retroactive | Yes (re-evaluated QTD) | No (only forward periods change) |

| Rep statement shows deductions | Yes | No |

| Setup complexity | Lower | Lowest |

Choose with deductions when you want retroactive plan changes to flow through and you do not mind reps seeing deduction lines on their statements; choose without deductions when you want cleaner statements and your plan does not include cash bonuses tied to attainment levels.

How Sales Cookie prevents double-payment

Whenever calculation periods overlap (which is inherent to YTD or QTD recalculation), there is structural risk of paying the same commission twice. Sales Cookie has three layers of protection:

- Automatic prior-payout lookup. When recalculating an overlapping period, the engine queries previously-released rewards on the same transactions and subtracts them from the new payout.

- Double-payment alerts. The system raises a warning whenever it detects the same commission could be paid more than once to the same payee over the same transaction. In a deliberate YTD/QTD setup these are false positives, and the alert can be silenced under Settings > Advanced.

- Detailed calculation logs. Every period’s calculation records, line by line, what was paid, what was deducted, and why. These logs are the audit evidence for retroactive adjustments.

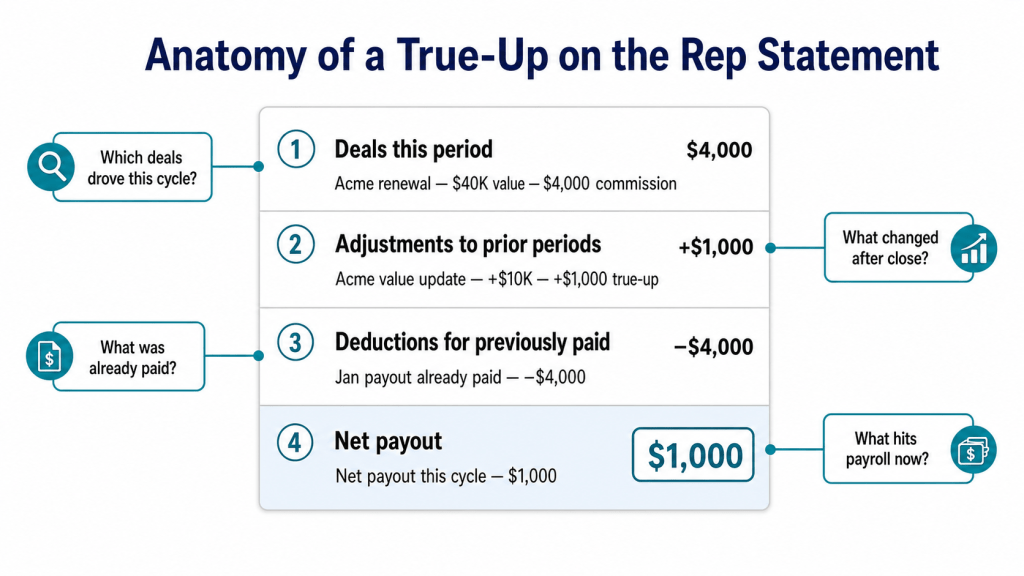

Designing the rep statement for true-ups

True-ups produce the highest dispute volume of any commission event, not because the math is wrong but because the rep sees a number that differs from what they expected and cannot tell why. A statement designed for true-ups solves the explanation problem upfront:

- Show the period’s headline commissions first. The reader’s first impression should be “what I earned this month.”

- Then show prior-period adjustments separately. A clearly-labeled section listing every deal where a prior amount changed and what the impact is on this month’s payout.

- Show deductions as a separate line. Not as “negative commissions” but as “previously paid: subtracted from this cycle.” The framing matters.

- Net to a single payout number at the bottom. The rep should be able to read the bottom-line number, then drill into the math if curious.

- Surface the cause. Label each true-up with what changed (amount, date, ownership, plan rule) so the rep does not have to file a dispute to understand why their number moved.

Common failure modes and how to avoid them

| Failure mode | Mitigation |

|---|---|

| Silent overwrite of historical data without an audit trail | Force the source system to retain old versions, or shift to Pattern 1 (event log) for high-value deals. |

| Reps see a clawback they did not expect | Cap monthly negative net commission, spread the recovery across two or three months, and explain the cause on the statement. |

| Double-payment alerts get ignored because they are mostly false positives | Silence the alert intentionally when the plan is correctly configured for overlapping calculations; do not let it accumulate as noise. |

| Plan rule changes mid-year retroactively change past payouts | Decide deliberately: either announce that mid-year changes are retroactive and use deductions, or freeze old periods and run a new plan version forward only. |

| Effective date changes are not policed by Sales Ops | Require manager approval for any backdated effective date; surface it on the audit log. |

| Refunds arrive multiple periods later and force a large clawback | Maintain a small contingency reserve (held back from each payout) to absorb refund clawbacks without affecting current pay. |

Bottom line

Sales data changes after the fact, every cycle, in every organization. The cost of pretending it does not is paid in commission disputes, audit findings, and lost trust between Sales and Finance. The cost of handling it deliberately is one decision (which of the three patterns fits your data architecture) and one piece of plan configuration (effective dates, deduction settings, and rep-statement labels). Sales Cookie’s engine handles all three patterns natively. The discipline that has to come from the team is choosing which one and then communicating it consistently to reps.

See the deduction logic in action. Our team will walk you through whichever of the three patterns fits your data architecture and configure a plan that handles true-ups cleanly. Book a personalized demo. Pair this article with our pay-when-you-get-paid guide, our crediting engine deep dive, and our commission disputes anatomy.

Sources: Sales Cookie – Dealing with ever-changing sales data; Sales Cookie – What are deductions; Sales Cookie – Monthly plan with QTD attainment recipe; FASB ASC 606.