Reading time: about 11 minutes. A 14-question, four-section scorecard for deciding whether your commission setup is healthy, walking-wounded, or actively losing you reps and revenue. Plus the four hard triggers that mean the spreadsheet has to go this quarter.

Most sales operations and finance leaders already know, in some general way, that their commission process could be better. They are also reluctant to do anything about it until something obvious breaks. The result is that commission programs limp along on spreadsheets and tribal knowledge for years longer than they should, accumulating disputes, errors, attrition risk, and audit exposure the entire time. The problem is not motivation. The problem is that there is no shared definition of “bad enough to fix now.”

This article offers one. It walks you through the same 14-question scorecard that powers the Sales Cookie self-assessment, organized into four sections that together capture the entire commission lifecycle. Each section produces a letter grade from A (everything is fine) to E (you are bleeding). The article explains exactly what each question is testing for, what a “wrong” answer says about your operation, and at what combined grade you should stop deliberating and start automating.

How the scoring works

The scorecard is deliberately simple. Each section has three or four yes/no questions. Each question contributes one point to the section’s “concern count” when answered in the wrong direction. The concern count maps to a letter grade and a color on a five-level scale.

| Concern count | Grade | Color | Circle level (UI) | What it means |

|---|---|---|---|---|

| 0 | A | forestgreen | full | Healthy. Reassess in 12 months. |

| 1 | B | darkorange | threeQuarters | One soft spot. Track it, do not ignore it. |

| 2 | C | darkorange | half | Visible cost to the business. Plan the fix. |

| 3 | D | orangered | quarter | Material risk. Move within the next quarter. |

| 4 or more | E | orangered | empty | Acute risk. You are likely losing reps and money. |

Two practical notes before you score yourself. First, the questions are written in mixed polarity: some count when the answer is “yes” (because doing the thing is a sign of trouble, like “do you manually send commission spreadsheets?”), and others count when the answer is “no” (because not doing the thing is a sign of trouble, like “can your reps access their statements online?”). The scoring rules below spell out which direction is the concerning one for each question. Second, no section is more important than another in isolation, but the combination matters a great deal. A team that scores A on overhead but E on rep satisfaction is in a different kind of trouble than one with the opposite pattern. We come back to combined-grade interpretation at the end.

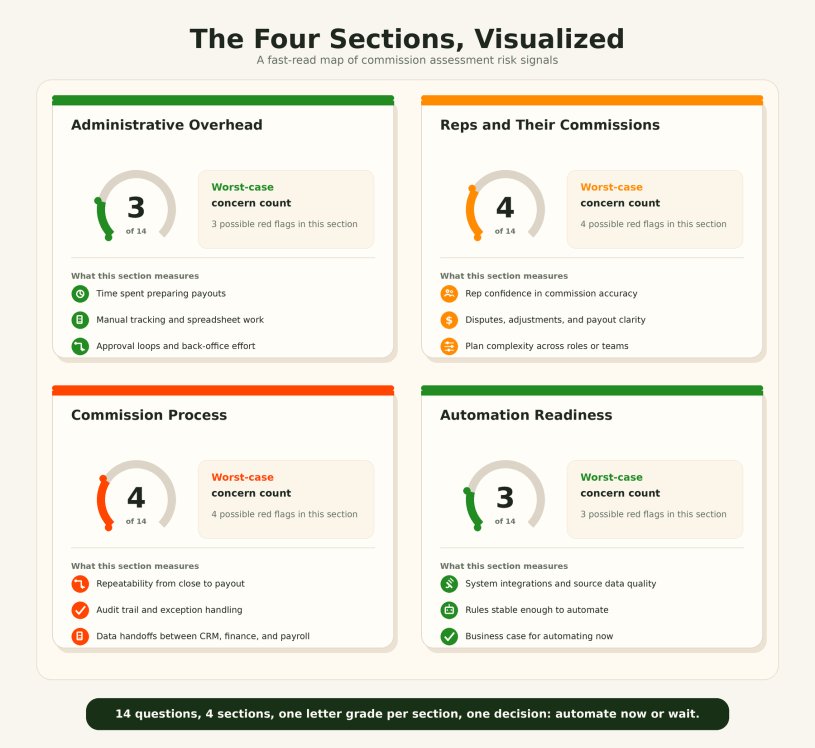

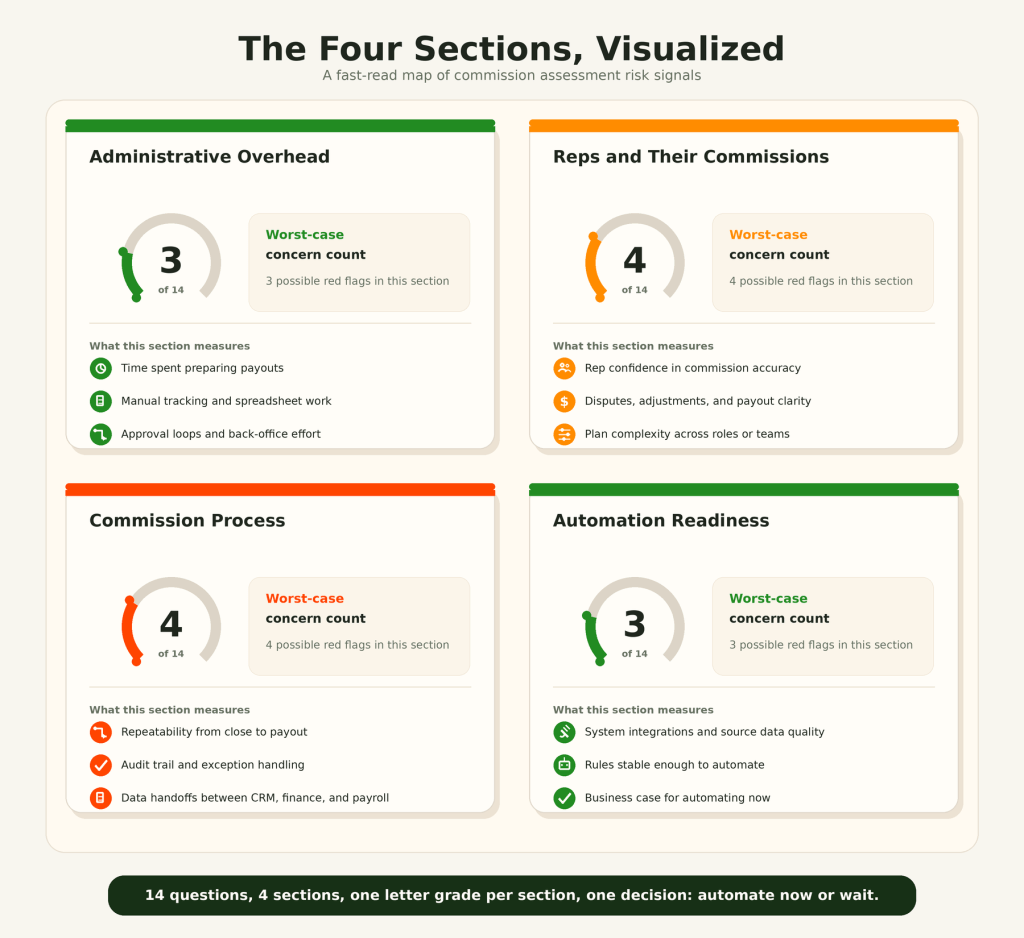

Section 1: Your administrative overhead

This section measures whether commissions are quietly eating your finance and sales-ops calendars. Three questions, all of which count against you when the answer is “yes.”

| Question | Counts against you when | Why it matters |

|---|---|---|

| Do you manually generate and send commission spreadsheets? | Yes | Spreadsheet authorship is the single highest-leverage operational fix in commissions. Industry research on spreadsheet error rates puts the cell-level mistake rate at roughly 1 percent in non-trivial financial models. Multiply that by hundreds of rows per cycle. |

| Do you have a large volume of commission disputes or inquiries? | Yes | Disputes are the visible tip of a much larger trust problem. Each one costs roughly 20 to 40 minutes of finance and sales-ops time, plus an unmeasured cost in rep confidence. |

| Is managing commissions taking too much of your time? | Yes | If the people who own commissions can articulate “this is too much,” there is no upside in waiting for the situation to deteriorate further. The cost is already being paid; it is just hidden in cycle-time and morale. |

The threshold to act on this section is low. One concern means you should benchmark how many hours per month go into commissions; two means the case for automation is already paying for itself; three means you are running an unfunded part-time commissions team out of someone’s existing job.

Section 2: Your reps and their commissions

This section measures whether the experience your reps have with their compensation is helping them sell, or actively distracting them. Four questions, mixed polarity.

| Question | Counts against you when | Why it matters |

|---|---|---|

| Do your reps waste time self-calculating commissions? | Yes | Shadow spreadsheets at the rep level are diagnostic: they mean reps do not trust the official number, and the team is paying for the same calculation twice (once by ops, once by every rep on every cycle). |

| Can your reps access their commission statements online? | No | PDF-by-email and Excel-by-attachment add latency, audit gaps, and version-control problems. A self-serve statement is the single feature reps consistently rate as most important. |

| Are your reps usually paid their commissions on time? | No | Late commissions are an extremely strong predictor of rep churn. Survey work in sales-comp research routinely shows late payment as a top-three driver of voluntary departures. |

| Have you lost reps because of commission-related issues? | Yes | If even one departure cited commissions in the exit interview, the cost has already exceeded the lifetime price of automation. Average loaded cost to replace a quota-carrying rep is in the high five figures to low six figures. |

This is the section where the cost of inaction is most asymmetric. Spreadsheet overhead grows linearly; rep attrition compounds. A single A-player departure for a commission-related reason is often more expensive than five years of every other line item on this scorecard combined.

Section 3: Your commission process

This section measures the underlying machinery: change agility, error rate, legal protection, and accounting compliance. Four questions, mixed polarity.

| Question | Counts against you when | Why it matters |

|---|---|---|

| Can you easily make changes to your commissions? | No | Plan agility determines how often you can experiment with rates, accelerators, and SPIFs. Teams that can change a plan in a day iterate. Teams that need a week stop trying. |

| Do you often experience commission calculation errors? | Yes | Calculation errors damage trust and create direct financial exposure. They also create a reverse audit problem: you cannot reliably restate prior periods if the formulas drift cycle to cycle. |

| Are your reps required to accept terms and conditions? | No | Without an electronic acceptance trail, every dispute becomes a “he said, she said” exercise. In states with strong wage-claim statutes, the absence of acknowledged plan terms is also a legal exposure. |

| Do your commissions comply with accounting requirements? | No | Revenue recognition rules require sales-incentive costs to be capitalized and amortized when the contract term is long enough. Audit firms will eventually ask for the supporting documentation, and “we have a spreadsheet” is not the answer you want to give. |

This section is the one that finance leaders should weight most heavily. Three of the four questions are about audit, legal, and accounting posture. A poor grade here does not just mean inefficiency; it means latent risk that materializes during diligence, audits, or an exit event.

Section 4: Your automation readiness

Three short questions that measure whether you are even in a position to automate yet. All three count against you when the answer is “no.” If this section grades poorly, the right move is usually not to automate immediately; it is to fix the prerequisite first.

| Question | Counts against you when | Why it matters |

|---|---|---|

| Do you have a system (for example, a CRM) tracking your sales? | No | Automation needs an authoritative source of truth for transactions. Without a CRM or equivalent, automation has nothing to pull from and you will spend the project budget on data plumbing instead. |

| Is your existing commission structure well-defined? | No | Automation does not invent plan design. If your current plan is ambiguous or improvised, the first job is to write it down clearly; only then can it be automated reliably. |

| Do you have 8 or more payees? | No | Below roughly 8 payees, the ROI math for automation gets thinner. There are exceptions (complex plans, high turnover, audit-heavy industries), but as a default, very small teams often do fine with a tight spreadsheet for another year. |

The 8-payee threshold is not arbitrary. It is the inflection point where total commission-admin hours per cycle typically exceed what one person can do alongside other duties, and where the marginal cost of one more payee on a spreadsheet starts to rise faster than the cost of putting them on a platform. Below that line, the question is “should we tidy up the spreadsheet?” Above it, the question is “which platform?”

Reading your combined scorecard

The four section grades together describe one of a handful of recognizable operating profiles. Match yours to the closest description and the recommended action falls out naturally.

| Profile | Section grades | Recommended next move |

|---|---|---|

| Healthy and steady-state | A or B across all four sections | Reassess annually. No urgent change required. |

| Overhead-heavy but otherwise OK | C or D on overhead; A or B elsewhere | The ROI from automation here is almost pure time savings. Quantify the hours, build a one-page business case. |

| Reps unhappy, ops calm | C, D, or E on reps; A or B on overhead | You have a trust problem, not a workload problem. Prioritize self-serve statements and on-time payment first. |

| Process-fragile and risk-exposed | D or E on process; mixed elsewhere | Treat as audit and legal exposure first, efficiency project second. Move within the quarter. |

| Not ready to automate yet | D or E on automation readiness | Fix the prerequisites first: a system of record, a written plan, or wait until you cross 8 payees. |

| Critical across the board | D or E on three or four sections | Stop deliberating. Every cycle you do not change is paying a recurring cost in time, trust, and attrition. |

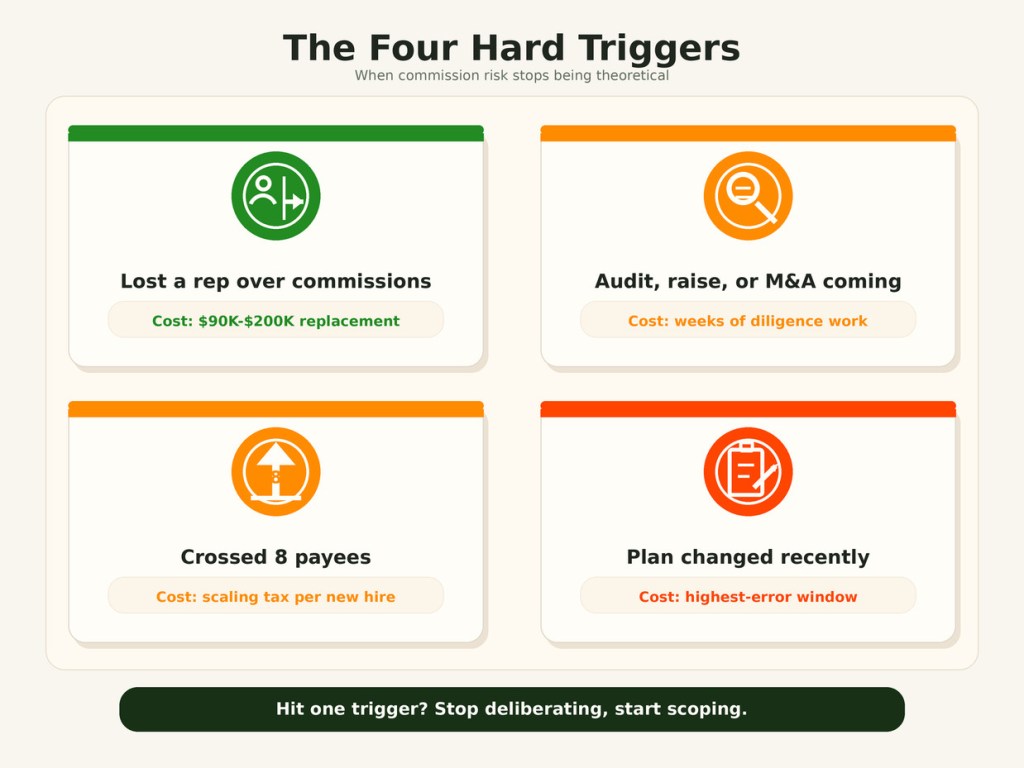

The four hard triggers that mean “automate now”

Even teams with mostly green grades have specific events that should override the default “wait a bit longer.” If any of the following are true for you, the question of timing is already answered.

- You have lost a rep in the last 12 months for commission-related reasons. The fully loaded cost of replacing a quota-carrying rep, including ramp time and lost pipeline, is almost always larger than three to five years of commission-platform fees. One named departure justifies the project.

- You are heading into an audit, a fundraising round, or a sale. Diligence teams will ask to see the calculation methodology, the plan acceptance records, and the audit trail. “We use a spreadsheet” is fine for the first conversation and a problem by the fourth. Get the documentation in order before someone external is asking.

- You crossed eight payees this year, or expect to in the next two quarters. Below eight, manual is defensible. Above eight, manual stops being a cost-saving choice and becomes a tax on the operations team that scales with every new hire.

- You changed your plan structurally in the last six months. Plan changes are the highest-error moments in any commission program. If your reps are operating on a plan that has not been thoroughly stress-tested, the chance of a calculation error in the next two cycles is much higher than baseline, and the cost of one error in trust is substantial.

If none of the four triggers apply and you are mostly A or B across the four sections, you have permission to wait. If even one applies, the analysis is finished; the next conversation is “which platform” and “by when,” not “should we.”

What changes after you automate, by section

It is worth being concrete about which section grades typically move, how much, and how quickly. The pattern below is what we observe with customers in the first one to two cycles after going live.

| Section | Pre-automation | After automation | What drives the change |

|---|---|---|---|

| Administrative overhead | C or D | A or B | Spreadsheet elimination, dispute self-service, scheduled runs. |

| Reps and their commissions | C or D | B | Online statements, on-time payment, dispute resolution drops by 60 to 80 percent. |

| Commission process | C or D | A or B | Audit trail captured automatically, electronic plan acceptance, calculation log per payee. |

| Automation readiness | B or C | A | Plan formalization happens as part of implementation; CRM integration is in place by go-live. |

The fastest grade improvements show up in administrative overhead and process. Rep-experience grades take an extra cycle because reps need a complete period in the new system before their perception catches up to the underlying reality. Automation-readiness grades almost always flip to A because formalizing the plan is part of the implementation work itself.

Questions you should be able to answer in five minutes

Before you take the full scorecard, run yourself through these. If any answer takes more than a minute, that is itself a finding.

- How many hours per month does your team spend on commission administration, end to end? If you cannot estimate within 25 percent, you do not have visibility into your own overhead.

- What is your dispute rate (disputes per 100 statements) for the last two cycles? If you do not measure it, you cannot manage it.

- What percentage of your reps have logged in to look at their own commission statement in the last 30 days? Below 50 percent is a trust signal worth investigating.

- Have you ever had to restate a prior period’s commissions? If yes, how long did it take, and what did it cost in trust?

- When was the last time you tested a new accelerator or SPIF? If the answer is “more than 6 months ago,” your plan agility is constraining your strategy.

Take the full Sales Cookie self-assessment when you have five minutes. It produces the four letter grades and a color-coded summary so you can see at a glance which sections need attention. The questions are exactly the 14 walked through above; the scoring is exactly the model described in this article.

What to do next

If you took the assessment and landed mostly in A or B territory, save the results and reassess in a year. If you are in C, build the business case but do not panic. If you are in D or E on any section, the conversation has moved from “should we automate” to “what is the fastest path to going live.” We are happy to help with that path. Book a 30-minute call and we will walk you through the scorecard, the data behind the grade thresholds, and a concrete plan for moving up the scale within one or two cycles.

Related reading

- Why it is crazy not to automate commissions

- The huge ROI of commission software

- Our process to automate your commissions

- Why only Sales Cookie can handle the most complex commission structures

- Quota attainment in 2024 vs 2025: what the data actually says

- Inside a crediting engine

Sources and notes

- The 14-question scorecard and color/grade mapping are taken from the Sales Cookie self-assessment: salescookie.com/Assess.

- Spreadsheet error-rate research: Raymond Panko, “What We Know About Spreadsheet Errors” and EuSpRIG spreadsheet horror stories.

- Industry benchmarks on rep attrition and quota: Salesforce State of Sales and Harvard Business Review, Motivating Salespeople.

- Revenue recognition treatment of sales commissions: FASB ASC 606.

- Wage-claim exposure for commissions: California DLSE FAQ on commission wages.