Reading time: about 13 minutes. A working reference for finance leaders, controllers, and audit-prep teams capitalizing sales commissions under ASC 606 / 340-40.

Most SaaS finance teams know they should capitalize sales commissions on multi-year contracts. Far fewer can hand an auditor a clean schedule that proves it. The gap between knowing and doing usually lives inside a workbook nobody wants to open. This guide closes that gap. It walks through what ASC 340-40 actually requires, when commissions can stay as period expense, how to build the amortization schedule, and where the SEC keeps finding issuers in comment letters.

What ASC 340-40 actually says

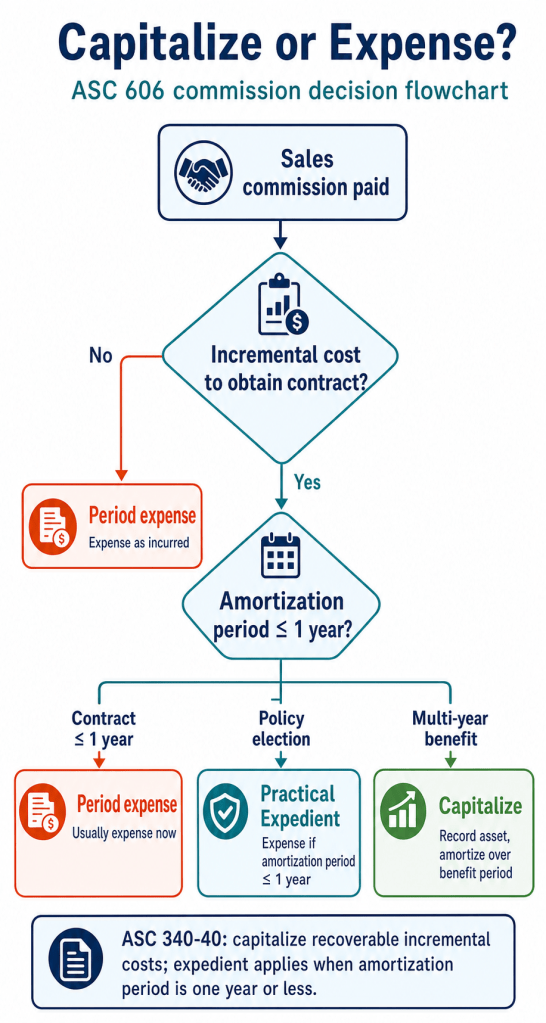

ASC 340-40 is the cost-to-obtain-a-contract subsection of ASC 606. It tells you that incremental costs of obtaining a customer contract, paid only because the contract was signed, must be capitalized as an asset and amortized over the period the company expects to benefit from those costs. For most B2B SaaS contracts, that means commissions on new logo deals, including bonuses tied directly to those deals.

Both Deloitte’s DART revenue recognition library and KPMG’s revenue recognition handbook walk through the specific tests. The two questions that decide most cases are simple. First, would you have paid the commission if the contract had not been signed? If no, it is incremental. Second, what is the expected customer life, including reasonably anticipated renewals? That is the amortization period.

Period expense vs. capitalize: the decision matrix

| Scenario | Treatment | Why |

|---|---|---|

| 12-month deal, paid commission at booking | Period expense (practical expedient) | Amortization period would be one year or less |

| 36-month deal, paid commission at booking | Capitalize, amortize over expected customer life | Multi-year benefit, incremental cost |

| Renewal commission on existing customer | Capitalize over the renewal term only | Renewal benefit horizon is typically the renewal term |

| Sales manager override on team performance | Generally capitalize | If tied to specific contracts, it is incremental |

| SDR-stage spiff on opportunity creation | Period expense | Paid regardless of close, not incremental |

| President’s club / annual bonus pool | Period expense | Tied to overall performance, not individual contracts |

| Implementation services bundled with subscription | Capitalize (carefully) | If commission is on the bundled package, allocate |

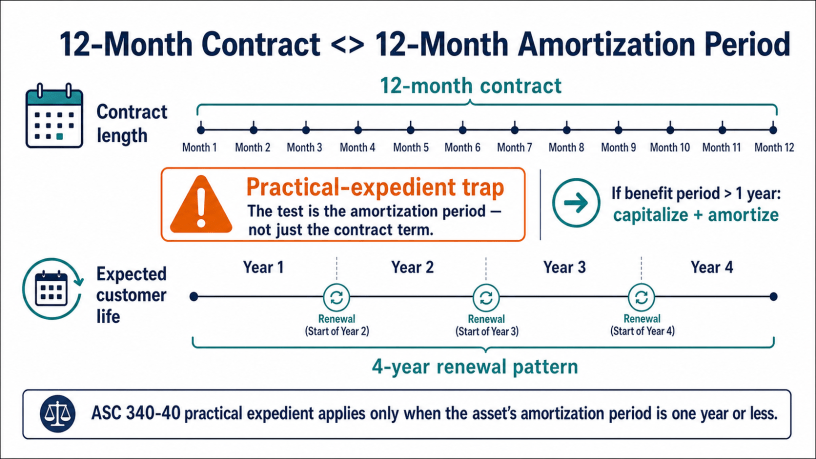

The practical expedient (and why it traps people)

ASC 340-40 includes a practical expedient: if the amortization period would be one year or less, you may expense the commission as incurred. It sounds simple. The trap is the word “amortization period,” which is not the same as the contract length. It is the period the company expects to benefit, including renewals.

For a SaaS product where the average customer renews three or four times, even a 12-month initial contract has an expected benefit period much longer than one year. Most public SaaS issuers cannot use the practical expedient on new logo commissions for that reason. The SEC has cited multiple registrants in comment letters specifically for inappropriate use of the expedient. KPMG’s handbook notes this is one of the most common findings in revenue recognition reviews.

How to determine the amortization period

The amortization period must reflect the period over which the asset will be consumed, which generally tracks the expected customer relationship. Three accepted methods, each with different audit risk:

- Cohort-based estimate. Use historical churn data to compute the average tenure of customer cohorts. Most defensible. Requires at least three to four years of cohort history.

- Useful life of the underlying technology. Acceptable when the product itself has a known refresh cycle (typical 3 to 7 years for enterprise platforms).

- Contract term plus anticipated renewals. Used when historical data is thin. The auditor will ask how renewal expectations were estimated.

Whatever method you choose, document the assumption and apply it consistently. Switching methods between periods is a red flag.

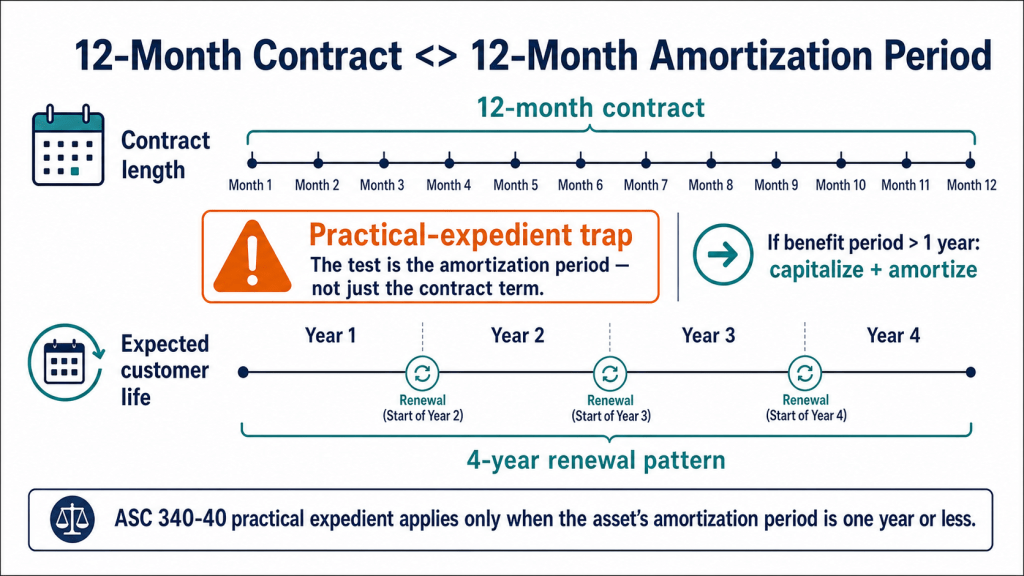

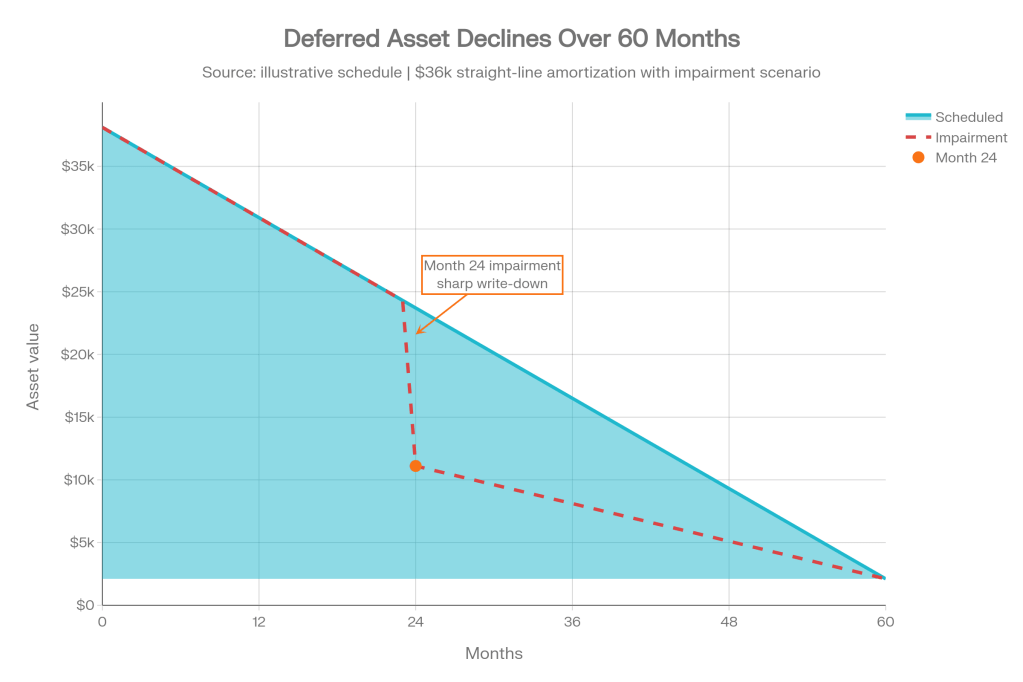

A worked example

A SaaS rep closes a 36-month contract with $120,000 ARR. They earn a 10 percent commission at booking, totaling $36,000. The company has determined an expected customer life of 60 months based on cohort retention data.

| Period | Action | Amount | Account |

|---|---|---|---|

| Month 0 (booking) | Capitalize commission | $36,000 | Dr. Deferred Commission Asset / Cr. Commission Payable |

| Month 1 | Amortize ($36,000 / 60) | $600 | Dr. Sales Commission Expense / Cr. Deferred Commission Asset |

| Months 2 through 60 | Same monthly amortization | $600 each | Same accounts |

| If customer churns at month 24 | Impair remaining balance | $21,600 | Dr. Impairment / Cr. Deferred Commission Asset |

| If customer renews at month 36 | Capitalize new renewal commission | New schedule | Same pattern, length = renewal term |

Where the SEC keeps finding issues

SEC comment letter trends point to a small list of recurring findings on commission capitalization. Both Deloitte and PwC publish quarterly comment letter summaries. The pattern across them:

- Practical expedient applied without support. Issuers asserting that amortization is one year or less without documenting the historical retention curve.

- Inconsistent amortization period across cohorts. Different reps, products, or segments capitalized over different lives without a clear policy.

- Missing impairment testing. No periodic check for customer churn or revenue decline that would impair the deferred asset.

- Renewal commissions not separately capitalized. Lumping new and renewal commission together over an inconsistent period.

- Vague disclosure. Descriptions that do not explain the amortization method or the average period actually used.

Implementation: what controllers actually need

An ASC 340-40 implementation should produce four artifacts that auditors expect to see, in any order, every quarter.

| Artifact | What it shows | Audit purpose |

|---|---|---|

| Capitalization policy memo | Decision rules, period determination, expedient use | Establishes consistent policy |

| Per-contract amortization schedule | Beginning balance, monthly amort, ending balance | Supports the deferred asset on the balance sheet |

| Cohort retention analysis | Evidence supporting the amortization period | Justifies the assumption |

| Impairment review | Customers churned vs. carrying balance | Triggers write-downs when needed |

What spreadsheets cannot do

Spreadsheet-based capitalization usually works for the first 12 months, then quietly degrades. The failure modes are predictable. Customer churn events do not propagate to the schedule. Renewals create new schedules that are not linked to the original. Plan changes mid-period fork the calculation. Impairment tests miss accounts because the underlying retention data is not joined. By year three, the deferred commission asset on the balance sheet is supported by a workbook nobody fully understands, which is exactly what audit committees no longer accept.

The fix is the same fix this blog has covered for other commission processes. Move the calculation into a system that stores per-contract data, links to the source CRM and billing system, and generates the schedule, amortization JE, and impairment review automatically. Sales Cookie connects to the source data, applies the policy rules, and pushes the period entries directly into your accounting system.

Bottom line

ASC 606 / 340-40 commission capitalization is not optional for SaaS issuers. Doing it well is a documentation problem more than a math problem. The companies that breeze through audit do four things: pick a defensible amortization period, apply it consistently, run impairment quarterly, and keep the schedule out of any single human’s head. Everything else is detail.

See how Sales Cookie generates per-contract amortization schedules and posts them directly to your GL. Start a trial or read our companion guide on automating commissions for QuickBooks.

Sources: FASB ASC 340-40; Deloitte DART Revenue Recognition; KPMG Revenue Recognition Handbook 2023; SEC Division of Corporation Finance guidance.