Reading time: about 14 minutes. The complete guide to designing, documenting, and operating sales commission clawbacks. For Sales Ops, Finance, HR, and Legal collaborating on policy.

Few topics generate more rep-leadership conflict than clawbacks. They are necessary, defensible, and routinely mishandled. The pattern is consistent: a deal closes, commission pays, the customer churns or refunds, and finance asks for the money back. What happens next depends almost entirely on whether the policy was written down before the deal happened. This guide walks through clawback types, the math, the legal framework, sample policy language, and the operational workflow that keeps the process clean.

The four types of clawback

| Type | Trigger | When to use |

|---|---|---|

| Refund clawback | Customer refund or credit memo within window | Universally applicable; standard for one-time payments |

| Churn / cancellation clawback | Customer cancels subscription before minimum tenure | SaaS and subscription businesses |

| Non-payment clawback | Customer never pays the invoice | B2B with longer payment terms; AR risk concentrated in commissioned reps |

| Termination clawback | Rep leaves the company within a defined window | Use sparingly; legally fragile in most U.S. states |

The first three are about commission expense matching the revenue actually collected. The fourth is about retention and is the riskiest legally. We will return to that one.

The math: proportional vs. full

Two calculation conventions cover the vast majority of B2B plans.

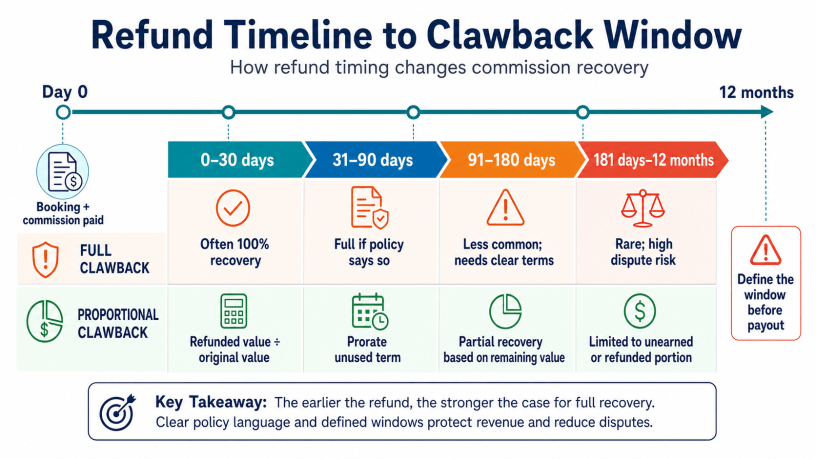

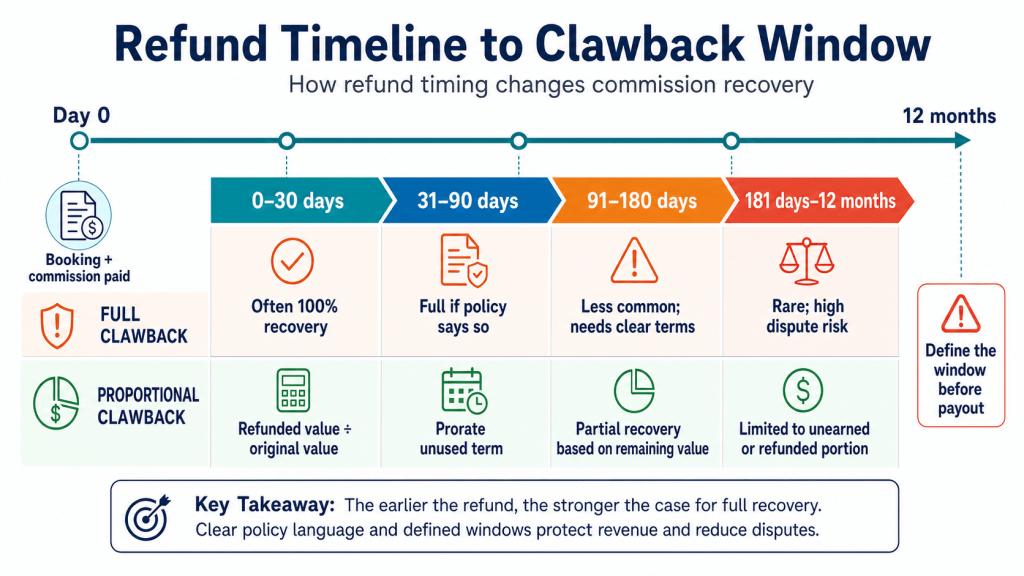

- Proportional clawback. Recover the percentage of commission corresponding to the unfulfilled portion of the contract. Most common and most defensible. Example: A rep earns $12,000 commission on a 12-month contract. The customer churns after 4 months. The clawback is $12,000 × (8 / 12) = $8,000.

- Full clawback (cliff). Recover the entire commission if churn happens within the lookback window. More aggressive. Should only be used with very short windows (60 to 90 days) and explicit rep acknowledgement.

| Scenario | Original commission | Proportional clawback | Full clawback (90-day cliff) |

|---|---|---|---|

| 12-month contract churns at month 2 | $12,000 | $10,000 recovered | $12,000 recovered |

| 12-month contract churns at month 6 | $12,000 | $6,000 recovered | $0 recovered |

| 12-month contract churns at month 10 | $12,000 | $2,000 recovered | $0 recovered |

| 36-month contract churns at month 12 | $36,000 | $24,000 recovered | $0 recovered (outside window) |

The legal framework: why clawbacks fail in court

State wage law treats earned commissions as wages, and most states have strict rules on when and how an employer can recover wages already paid. The defensibility of any clawback comes down to four factors:

- Was the clawback in writing before the rep earned the commission? If not, the answer almost always is “you cannot claw it back.”

- Did the rep specifically acknowledge the clawback in their plan document? A plan signature on each effective date is the strongest evidence.

- Is the clawback proportional and reasonable? Courts and labor commissioners look unfavorably on punitive clawbacks that exceed the actual harm.

- Is the trigger event objective? “At management discretion” is fragile; “if the customer refunds within 90 days” is robust.

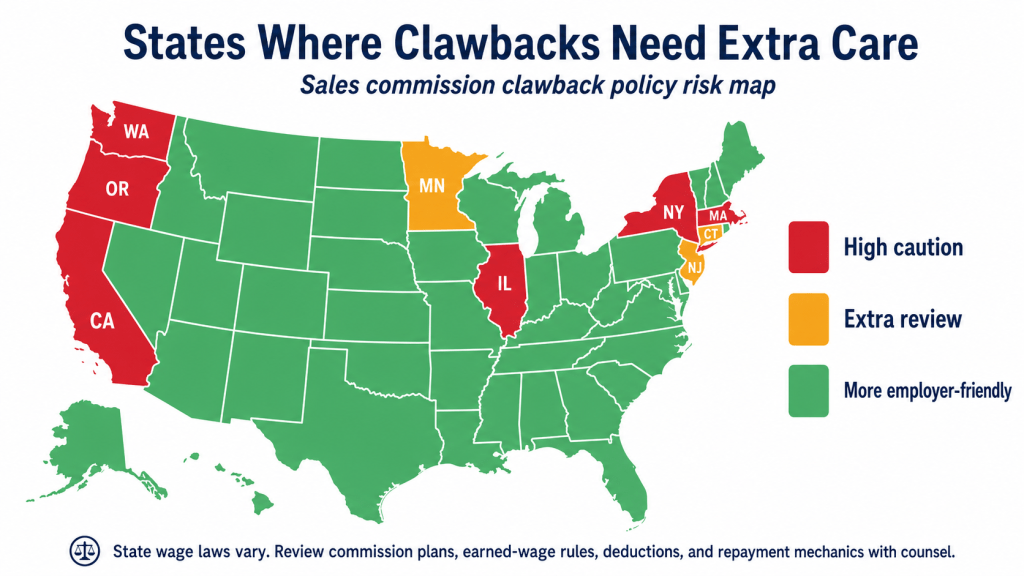

State-by-state highlights

| State | Statute / framework | What it means for clawbacks |

|---|---|---|

| California | Labor Code 2751 | Written commission agreement required. PAGA exposure for ambiguous plans |

| New York | NY Labor Law Section 191 | Wage timing requirements; written agreement strongly advised |

| Massachusetts | MA Wage Act | Treble damages on improper wage withholding; clawbacks face high scrutiny |

| Illinois | Sales Representative Act | Final commissions must be paid within 13 days of termination; treble damages possible |

| Texas / Florida | Common law contract | More employer-friendly, but written acknowledgement still strongly advised |

| Washington / Oregon | Wage and Hour statutes | Recoverable draws and termination clawbacks especially fragile |

This is general framing, not legal advice. A clawback policy operating in multiple states needs review by employment counsel for each jurisdiction.

Sample policy language

Use the language below as a starting point, customize with your counsel, and place it in the plan document each rep signs at the start of every plan period.

Refund Clawback. If a customer is granted a refund or credit memo against an invoice for which Commission was previously earned and paid, the Commission attributable to the refunded portion shall be recovered from future Commission earnings. Recovery shall be proportional to the refunded portion of the original invoice and shall apply only to refunds processed within twelve (12) months of the original payment date.

Churn Clawback (Subscription). If a Customer cancels their subscription within the first one hundred eighty (180) days of the effective Contract Start Date, the Commission earned on the original booking shall be subject to recovery. Recovery shall be calculated as: (Original Commission) × (1 minus (Days Active / 180)). Recovery shall be applied as a deduction against the rep’s next earned Commission and shall not result in a negative balance carrying forward beyond the second subsequent commission period.

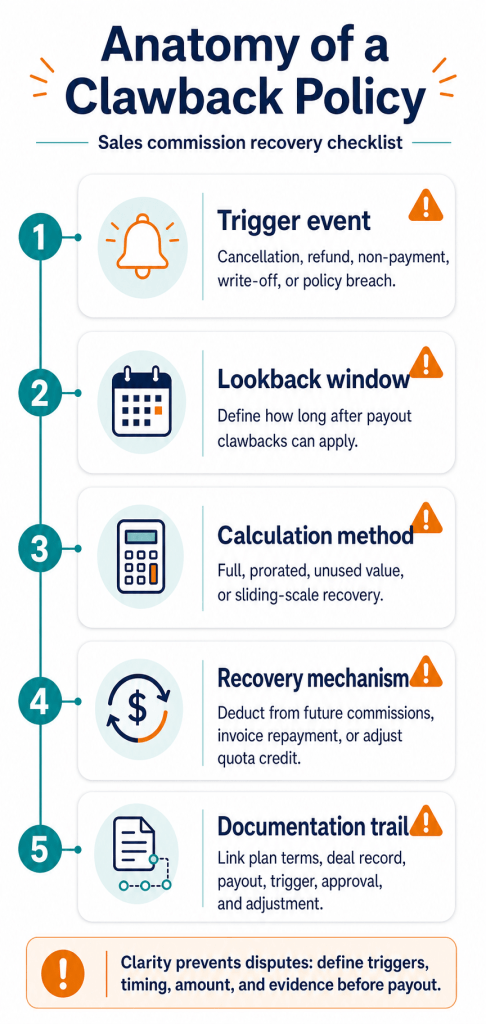

Documentation. Each clawback shall be documented in the rep’s commission statement with the trigger event, original deal reference, calculation, and net adjustment clearly identified.

The operational workflow

Clawback execution fails when it lives in a separate spreadsheet from the original commission calculation. The reconnection should happen automatically, with the audit trail preserved.

- Trigger detection. The system identifies a refund, credit memo, or cancellation event from the source-of-truth system (CRM, billing, or QuickBooks).

- Eligibility check. The system confirms the original deal was inside the clawback window and that commission was actually paid (not just earned).

- Calculation. The system applies proportional or full clawback per policy.

- Statement adjustment. The clawback flows to the next commission statement as a clearly labeled adjustment, with reference to the original deal.

- Notification. The rep receives notice of the clawback before the statement is finalized, with appeal rights.

- Audit log. The trigger, calculation, and adjustment are stored with timestamp and version, accessible during audit.

Accounting treatment

Under ASC 606 / 340-40, clawbacks affect both the commission expense and the deferred commission asset. Two patterns:

- Refund within the period. Reverse the booked revenue, the commission expense, and (if capitalized) impair the remaining deferred commission asset.

- Churn after the period. Reverse the unrecovered portion of the commission expense and impair the remaining deferred asset. The rep statement adjustment posts as a credit against future commission payable.

Both patterns require linkage between the original transaction and the clawback event in the journal entry detail. Auditors will trace this in any Series A or later company.

Common mistakes to avoid

- Adding clawbacks mid-year. Cannot be applied retroactively. New clawback rules apply to deals booked after the new policy effective date.

- Stacking proportional with full clawback. Pick one. Reps cannot reasonably model their comp under hybrid rules.

- Termination clawbacks longer than 90 days. Legally fragile in most states. Use a recoverable draw structure instead if you need to manage rep retention.

- Recovering through final wages. Most states prohibit deducting clawbacks from a rep’s final paycheck without explicit written authorization. Litigation magnet.

- Surprise clawbacks. Rep finds out via paycheck. Always notify in advance with appeal rights.

Bottom line

A clawback policy is a contract term, not an administrative footnote. The companies that handle this well share three habits: they write the rules down, they enforce the rules consistently, and they automate the calculation so reps and finance see the same number on the same day. The companies that handle this badly end up in the kinds of cases we covered in our nightmares roundup.

Want to see how clawback automation works against your CRM and billing data? Try Sales Cookie or read our commission structures guide for how clawbacks fit into broader plan design.

Sources: California Labor Code 2751; U.S. Department of Labor Wage and Hour Division; FASB ASC 340-40; The Recorder, Oracle PAGA settlement (2025).