Reading time: about 14 minutes. The six concrete risks of running commissions in spreadsheets, what the research actually says about error rates and rep churn, and an honest cost calculation finance leaders can run on their own numbers.

Ask any finance leader running commissions in spreadsheets whether the system is working, and the answer is usually some version of “it is fine, we manage.” Ask the rep on the other end of that spreadsheet, and the answer is different. Ask the auditor, and the answer is different again. Ask the GC after the first wage-and-hour suit, and the answer becomes very different. The reality of manual commissions is that the cost is real, but it is paid in many small invoices that no single budget owner sees in one place: extra finance headcount, occasional rep clawbacks, slow close cycles, lost top performers, and the rare but very expensive class-action exposure.

This article walks through the six concrete risks of not automating commissions, with the research and math behind each. It is written for a buyer who suspects automation is worth it but has not yet built the internal case. By the end you should have enough numbers to run the calculation on your own organization and decide whether the status quo is actually a bargain or just an invisible expense.

Are you really sure the spreadsheet is working?

Before getting to the six risks, three honest questions. Take 30 seconds to answer each before reading the rest.

- If a rep emailed you tomorrow asking why a specific deal from three quarters ago was credited at $4,200 instead of $4,800, how long would it take you to produce a defensible answer with audit trail?

- If your finance lead won the lottery on Friday and disappeared, would anyone else in the company be able to run next month’s commission calculation accurately?

- If your auditor asked for the version of every plan in effect during Q2, plus every mid-period change, plus who approved each, could you produce it within a week?

If the answer to any of these is no, the spreadsheet is not actually working. It is working until it stops. The cost is denial, paid in lump sums when something breaks.

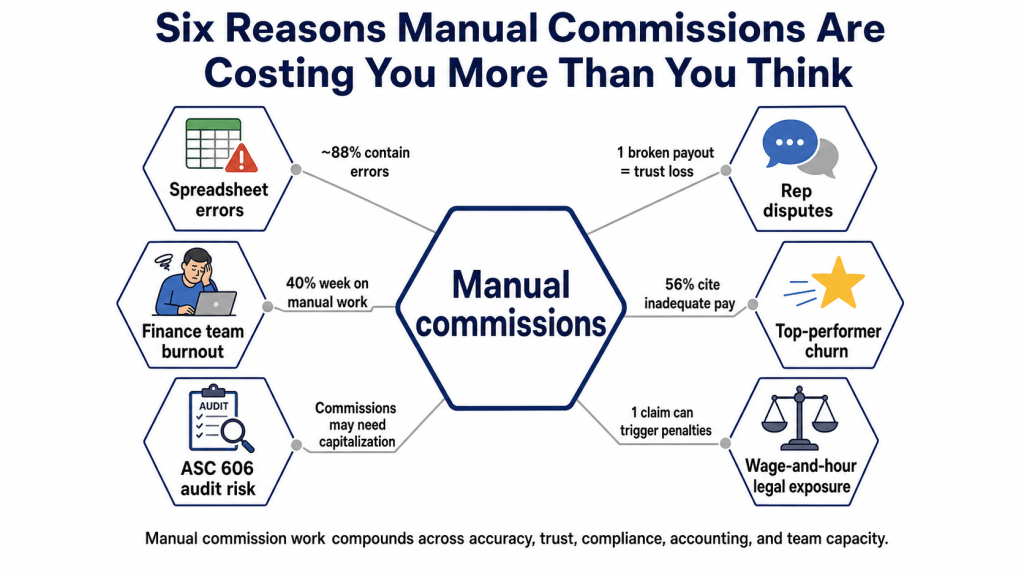

Risk 1: Spreadsheet errors are not rare, they are the baseline

The most-cited research on spreadsheet error rates comes from Professor Raymond Panko at the University of Hawaii, summarized by the European Spreadsheet Risks Interest Group. The headline finding: in field audits of operational spreadsheets, more than 90 percent contain errors, and only a fraction are caught by review. EuSpRIG’s research summary states that “the majority (greater than 90 percent) of spreadsheets contain errors” and that “spreadsheets are rarely tested,” so those errors persist (EuSpRIG, Research and Best Practice).

For most spreadsheet uses this is annoying but not catastrophic. For commission spreadsheets, every error compounds: an incorrect VLOOKUP in the tier table propagates through every rep on that tier, every quarter, until someone notices. Ventana Research, in their incentive-compensation surveys, has reported that the large majority of organizations using spreadsheets for incentive compensation experience errors that require time-consuming corrections. The relevant question is not “will my spreadsheet have errors” but “how long will it take to discover them, and what will it cost when I do.” For a deeper look at the error mechanics, see our spreadsheet horror stories article.

Risk 2: Disputes are expensive in time, not just money

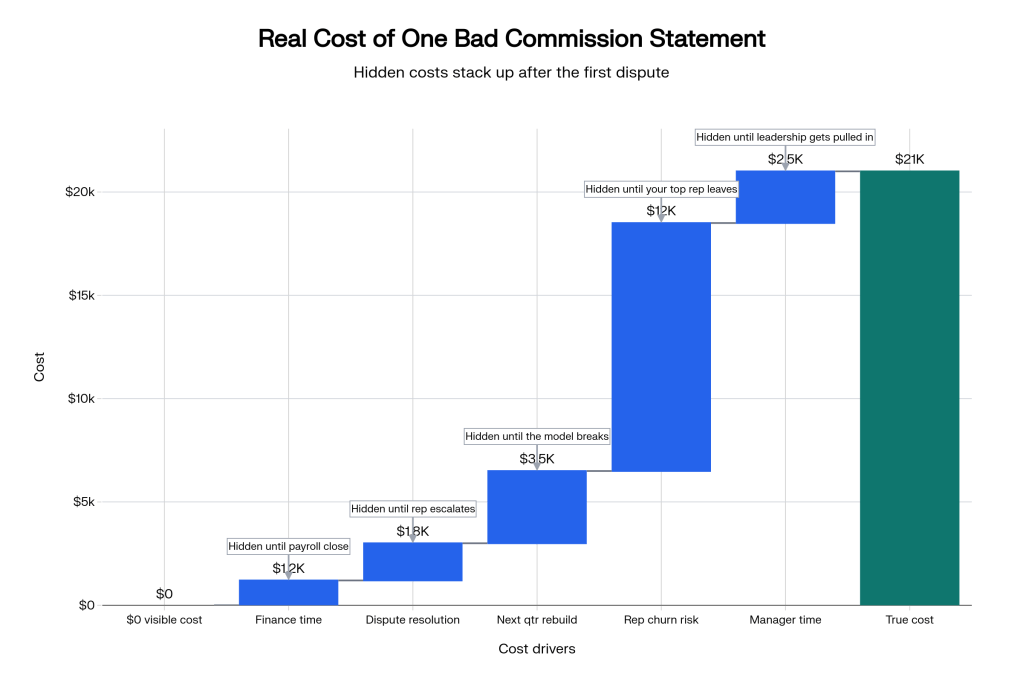

Industry research on commission disputes consistently lands in the same range: organizations running manual commissions see significantly more rep disputes than those with automated systems. The cost is not the dispute itself; the cost is the cycle the dispute starts. A rep questions their statement, finance pulls the source data, rebuilds the calculation, finds a discrepancy or confirms the number, writes a response, sometimes escalates to the rep’s manager, and finally closes the loop. Each cycle is hours of finance time for what should have been a five-minute audit-trail lookup.

Per a comprehensive market survey referenced by industry analysts, customers who automate commissions report over 40 percent fewer commission disputes. The implied finance-team time savings is substantial: if your finance team spends two days a month resolving disputes today, automation can reasonably take that to under a day. Multiply by 12 months and the team capacity recovered is non-trivial. Our hidden cost of running commissions manually article walks through the math in detail.

Risk 3: Commission errors cost you top performers

This is the risk most companies underweight. Sales reps live and die by their commission statement. If the statement is consistently wrong, late, or unexplainable, reps stop trusting it, and trust in the compensation system is the foundation of selling motivation. Industry surveys repeatedly find that a meaningful percentage of companies lose part of their sales force to commission errors every year or two. The departing reps are disproportionately top performers, because top performers have the most to lose from miscalculation and the most options elsewhere.

The cost math is brutal. A fully-ramped account executive typically takes 6 to 12 months to ramp and represents 1.5x to 2x their salary in opportunity cost over the ramp period. Losing one top AE because their commissions were repeatedly wrong is a six-figure loss that does not appear on any line item. Multiply by the number of disputed quarters the rep tolerated before leaving, and the cost of “managing it manually” becomes obvious.

Risk 4: Wage-and-hour exposure is real and growing

Commission disputes that go unresolved internally can become legal disputes externally. In the United States, state wage-and-hour laws treat earned commissions as wages, and underpayment, late payment, or unilateral plan changes that retroactively reduce earned commissions can trigger penalties, liquidated damages, and attorney fee shifting. California’s Labor Code section 2751 requires written commission agreements; states including Massachusetts, New York, and Illinois have their own enforcement regimes. A spreadsheet that cannot reliably produce the version of the plan in effect when each deal closed is a poor defense exhibit.

The question for a CFO or GC is not whether your current plan is unlawful. The question is whether, given a complaint, you can produce within reasonable notice: (1) the plan document signed by the rep, (2) the data showing each transaction, (3) the calculation tying each transaction to a payout, (4) the audit log of any plan changes mid-period, and (5) the approval trail for each change. Manual processes can sometimes assemble four of those five; rarely all five, and almost never quickly.

Risk 5: ASC 606 commission capitalization makes audit complicated

Since 2018, ASC 606 has required public and many private companies to capitalize incremental costs of obtaining contracts (the most common of which is sales commission) and amortize them over the period the customer benefit is recognized. If your amortization period would be one year or less you can apply the practical expedient and expense as incurred; otherwise, you have to schedule the amortization at the contract level. That schedule has to tie back to which commission was paid for which contract and how it should be treated when the contract is modified, renewed, or canceled.

Manually maintaining an ASC 606 commission amortization schedule against a separate commission spreadsheet is exactly the kind of cross-system bookkeeping that produces audit findings. The auditor will ask: how does your commission expense in the GL tie to the underlying deals and reps? Can you reproduce the calculation in real time? Are mid-period plan changes reflected in the amortization schedule consistently? Each “no” is a finding. Each finding is a remediation effort. See our crediting vs. payment article for how the credit-to-payment chain anchors ASC 606 cleanly.

Risk 6: Your finance team is burning out doing it

The least-discussed but most-felt cost is the toll on the people doing the manual calculation. Commission close week is unpleasant for the team running it: late nights, manual reconciliation, rep emails, fire drills when a deal lands in the wrong period. Senior finance team members spend close week on data entry and formula debugging instead of analytical work. Junior team members get the worst of it because the senior person has to focus on the trickier reps. Over time, this is one of the more common reasons sales-ops and revenue-ops hires leave.

Automation does not eliminate finance work; it changes the nature of it. Instead of running the calculation, the team reviews the calculation. Instead of building the spreadsheet, the team verifies the audit log. Instead of fielding disputes via email, the team checks the dispute log inside the tool. Same people, more strategic output, less burnout.

The six risks, summarized

| Risk | How it shows up | Order of magnitude |

|---|---|---|

| Spreadsheet errors | Wrong payouts, retroactive clawbacks, version drift | More than 90 percent of operational spreadsheets contain errors per EuSpRIG research |

| Rep disputes | Finance time pulled into reconciliation cycles | 40 percent or more dispute reduction reported with automation per industry surveys |

| Top-performer churn | Best reps leave first when statements lose credibility | Six figures per departure including ramp opportunity cost |

| Wage-and-hour legal exposure | State labor code claims for underpaid commissions | Penalties, liquidated damages, attorney-fee shifting |

| ASC 606 audit findings | Amortization schedule does not tie to commission ledger | Remediation cost, restated periods, qualified opinion risk |

| Finance team burnout | Close week dread, attrition in sales-ops and rev-ops | Replacement cost equals 1.5x salary per senior departure |

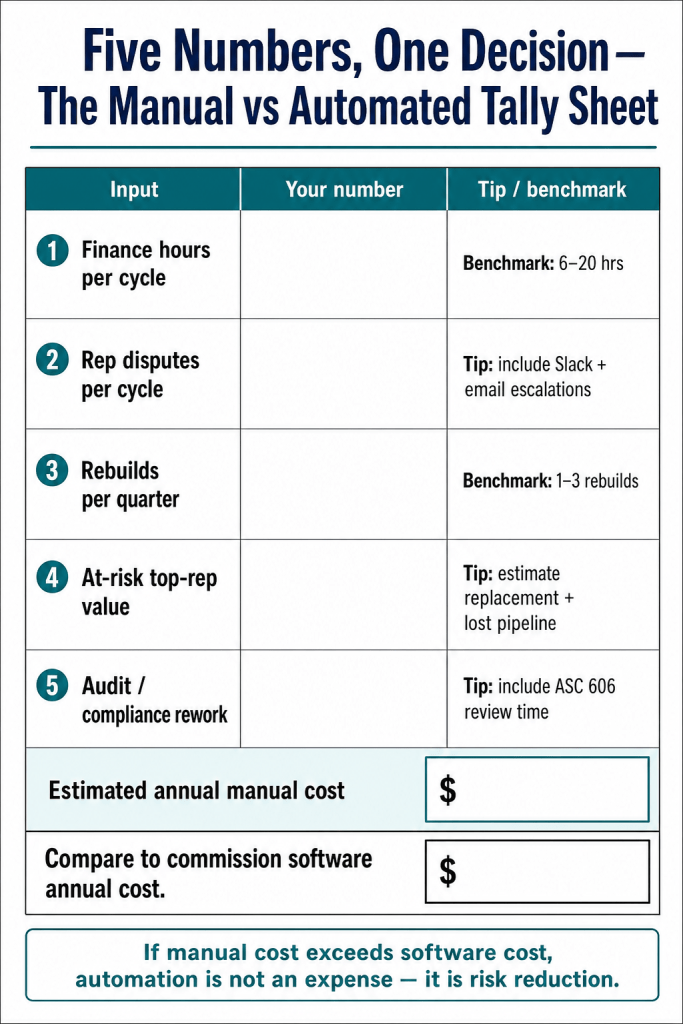

How to run the math on your own organization

Skip the vendor’s ROI calculator for a moment and run it yourself. Five numbers; pull them honestly from last year.

- Finance time on commissions. Hours per month per person, times salary, times 12. This is the most visible line item. Be honest about everyone who touches it, not just the named owner.

- Overpayment leakage. If you have ever run a clean recalculation against the actual rules, what percent of last year’s payouts were higher than they should have been? Conservative estimate is 1 to 3 percent of total commission spend. Industry data points to roughly 2 percent overpayment reduction with automation.

- Dispute resolution time. Average hours per dispute times disputes per quarter times the relevant finance hourly cost. Most organizations underestimate this by half because the cycles are scattered across email.

- Rep churn cost. If even one top AE leaves per year and you believe statement quality was a factor, divide that fully-loaded cost across the program. Most CFOs find this dominates the calculation.

- Audit and legal contingency. Hard to quantify until a claim arrives; build in a small annual reserve and a much larger but lower-probability tail.

Add the five up. Compare to commission software cost. For most organizations above 25 reps, the answer is not close. For organizations above 100 reps, the cost of not automating routinely runs 5x to 20x the cost of automating. The TCO of spreadsheets article walks through one detailed example.

Three honest objections, and what we say back

If you have stayed on spreadsheets this long, you have already heard, and probably said, these objections. Here is what is true about each.

| Objection | Honest counter |

|---|---|

| “Our plans are too custom for software.” | Sales Cookie automates 99 percent of real-world commission structures including splits, overrides, draws, accelerators, clawbacks, and multi-source data. See our most-complex-plans article for the architecture that makes that true. |

| “We do not have time to implement.” | Most plans go from intake to first calculation in 2 to 4 weeks. Implementation runs incrementally, one plan at a time. Your first plan configuration is free. |

| “Software is more expensive than people think.” | Run the five-number calculation above. The visible monthly subscription is almost always smaller than the invisible monthly cost of doing it manually. See our ROI article. |

| “We tried automation before and it did not work.” | The most common failure mode is hard-coded software that cannot handle exceptions. Sales Cookie was built with the explicit goal of supporting custom logic at every step of the calculation pipeline. |

The next step

Run the five-number calculation. Compare it to a real commission software quote. If the math does not work, stay on spreadsheets and revisit in 12 months. If it does, the cost of waiting another year is whatever your highest number was, multiplied by 12 months you did not act. Book a 30-minute demo with one of our commission experts and bring a real plan document. We will walk through how the architecture handles your edge cases.

Related reading

- Our process to automate your commissions

- Why only Sales Cookie can handle the most complex commission structures

- The huge ROI of commission software

- The hidden cost of running commissions manually

- Spreadsheets vs. commission software TCO

Sources

- EuSpRIG, Research and Best Practice; Horror Stories

- Panko, R., What We Know About Spreadsheet Errors

- FASB, ASC 606 / 340-40 incremental costs of obtaining a contract

- California Department of Industrial Relations, Commission FAQ and Labor Code Section 2751

- Sales Cookie, Deconstructing sales commission software